Many entrepreneurs in iGaming and fintech mistakenly believe any bank account will suffice for their business operations. This misconception often leads to compliance headaches, payment processing failures, and stunted growth. A business bank account separates your personal and corporate finances while offering specialized tools designed for high-risk industries. Understanding how these accounts integrate with payment processing solutions can unlock sustainable banking relationships and operational success for your venture.

Table of Contents

- Key takeaways

- Understanding business bank accounts and their benefits

- Navigating payment processing challenges in iGaming and fintech

- Leveraging payment orchestration and open banking for cost savings and efficiency

- Choosing and managing your business bank account for fintech and iGaming success

- Explore Deincepstart: your partner in banking and business solutions

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| Separate finances | A business bank account keeps personal and company money apart to protect assets and simplify tax reporting. |

| Higher transaction limits | Business accounts are designed for commercial cash flow with higher limits and multiple authorized users. |

| FDIC insured | FDIC coverage up to $250,000 provides an extra layer of security beyond personal accounts. |

| Sub accounts for reserves | Set up separate sub accounts within your business account for operating expenses, tax reserves, and growth capital to prevent cash crunches. |

| Open banking boosts approvals | Open banking and payment orchestration help reduce costs and raise payment approval rates by improving data sharing and routing across providers. |

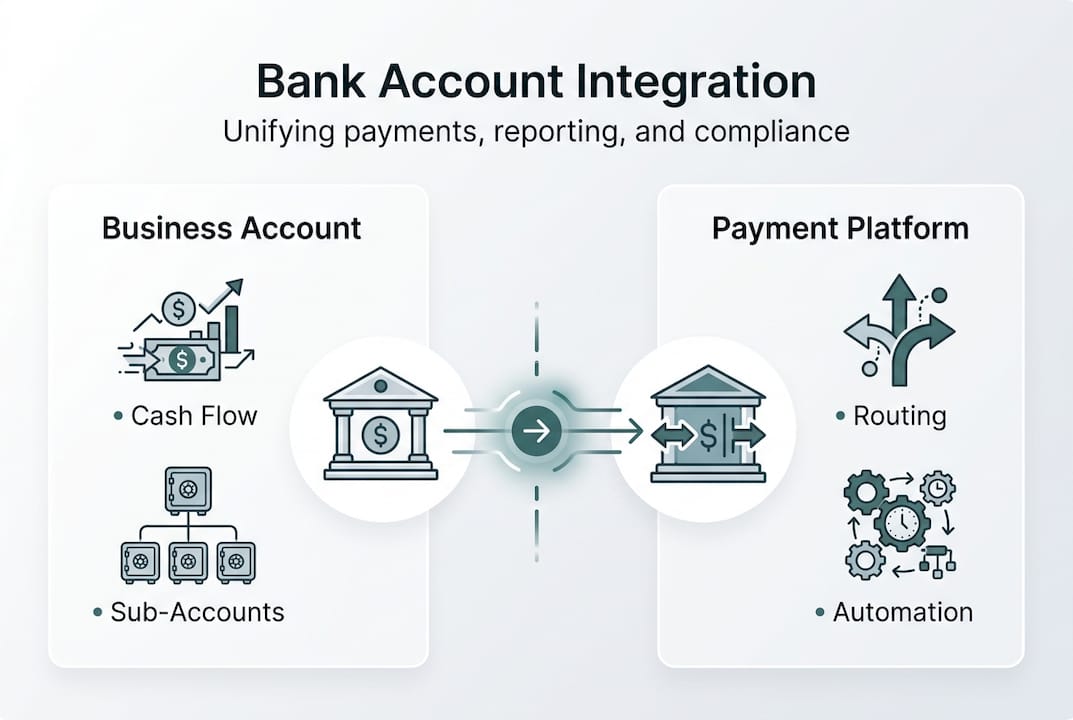

Understanding business bank accounts and their benefits

A business bank account is a dedicated financial account designed for managing your company's day-to-day transactions while separating business from personal finances. This separation isn't just good practice. It creates a legal firewall that protects your personal assets from business liabilities and simplifies tax reporting.

These accounts offer mechanics tailored for commercial operations. You get higher transaction limits that accommodate business-level cash flow, multiple authorized users with individual debit cards for your team, and seamless integration with accounting software like QuickBooks or Xero. FDIC insurance protects up to $250,000 separately from your personal accounts, giving you an additional layer of financial security.

For iGaming and fintech entrepreneurs, these features become mission-critical. Your business likely processes thousands of transactions monthly, requires multiple team members to access funds, and demands real-time visibility into cash flow. Standard personal accounts simply cannot handle this operational complexity. Business accounts provide transaction categorization, automated reconciliation, and detailed reporting that makes tracking your financial health straightforward.

The cash flow tracking features deserve special attention. You can monitor incoming payments, outgoing expenses, and working capital in real time. This visibility helps you identify payment bottlenecks, optimize timing for vendor payments, and maintain sufficient reserves for operational needs. When you integrate your banking & business solutions with payment processing platforms, you create a unified financial ecosystem that reduces manual work and improves accuracy.

Pro Tip: Set up separate sub-accounts within your business bank account for operating expenses, tax reserves, and growth capital. This internal segregation helps you avoid cash crunches and ensures you always have funds allocated for critical obligations.

Navigating payment processing challenges in iGaming and fintech

Payment processing in iGaming and fintech operates in a fundamentally different environment than traditional e-commerce. You need high-risk merchant accounts that can handle elevated fraud risks, higher chargeback rates, and complex regulatory requirements. Standard merchant accounts from mainstream payment processors will either reject your application or terminate your account after detecting gaming or high-risk fintech activity.

The mechanics of high-risk payment processing involve several specialized components. Multi-PSP routing distributes your transaction volume across multiple payment service providers, reducing dependency on any single provider and improving overall approval rates. Cascading automatically reroutes declined transactions to alternative processors, giving each payment multiple chances to succeed. These strategies are essential because approval rates in iGaming should hit 92-98%, compared to 95-99% in low-risk e-commerce.

Anti-fraud filters play a dual role in your payment infrastructure. They protect you from genuine fraud attempts while minimizing false declines that frustrate legitimate customers. You need to calibrate these filters carefully because iGaming typically experiences chargeback rates of 2-3%, compared to 0.5-1% for general e-commerce. Every percentage point above industry benchmarks costs you revenue and increases the risk of losing your merchant account.

Rolling reserves represent another unique challenge. Payment processors typically hold 5-10% of your transaction volume in reserve for 90-180 days to cover potential chargebacks and refunds. This impacts your working capital significantly. If you process $1 million monthly, you could have $50,000-$100,000 tied up in reserves at any given time. Factor this into your cash flow projections and maintain adequate operating capital.

Compliance risk handling extends beyond payment processing into your overall banking relationship. Banks evaluate your licensing status, operational jurisdiction, target markets, and regulatory track record. A mismatch between your corporate structure and operational reality creates red flags that can result in account closure. Your corporate banking solutions must align with your payment processing setup to maintain long-term bankability.

Pro Tip: Negotiate your rolling reserve percentage and release timeline during merchant account setup. Established businesses with clean processing history can often secure better terms than startups with no track record.

Leveraging payment orchestration and open banking for cost savings and efficiency

Payment orchestration platforms transform how you manage transaction routing and approval optimization. These systems increased approval rates by 23% for one gambling business processing $3.5 million monthly, saving $600,000 annually in recovered revenue. The mechanics involve intelligent routing algorithms that analyze transaction characteristics, PSP performance, and historical data to select the optimal payment path for each transaction.

Open banking represents a paradigm shift in payment processing economics. Trustly, a leading open banking provider, processed $100 billion in 2024 with 50% year-over-year growth and reduced card transaction fees by 50% for merchants. Instead of routing payments through card networks with their associated interchange fees, open banking connects directly to customer bank accounts through secure APIs. This eliminates intermediaries and dramatically reduces per-transaction costs.

The speed advantage of open banking cannot be overstated. Traditional card payouts take 3-5 business days to reach customer accounts. Open banking enables real-time payouts that complete in seconds or minutes. For iGaming operators, this improves customer satisfaction and reduces support inquiries about delayed withdrawals. For fintech companies offering marketplace or gig economy solutions, instant payouts become a competitive differentiator.

| Payment method | Transaction fee | Settlement speed | Chargeback risk |

|---|---|---|---|

| Credit/debit cards | 2.5-3.5% + $0.30 | 3-5 business days | High (2-3%) |

| Open banking (Trustly) | 1.0-1.5% | Real-time to 1 day | Very low (0.1%) |

| Bank transfers | 0.5-1.0% | 1-3 business days | Low (0.3%) |

| E-wallets | 2.0-3.0% | 1-2 business days | Medium (1-2%) |

Implementing payment orchestration and open banking requires strategic planning:

- Audit your current payment stack to identify approval rate gaps, high-cost processing routes, and customer friction points that orchestration can address.

- Select a payment orchestration platform that integrates with your existing PSPs and supports your target payment methods, including open banking providers.

- Configure intelligent routing rules based on transaction amount, customer location, payment method, and PSP performance metrics to optimize approvals and costs.

- Integrate open banking for both deposits and withdrawals, starting with markets where adoption is highest (UK, Nordics, Netherlands) before expanding globally.

- Monitor performance metrics weekly, including approval rates by PSP, average transaction costs, payout speed, and customer satisfaction scores to refine your strategy.

Treating banking as strategic risk means aligning your corporate structure, licensing, and operational setup with banking requirements from day one. Banks assess whether your business model, jurisdiction, and compliance framework create acceptable risk profiles. Misalignment leads to account rejections or sudden terminations that can cripple operations. Work with advisors who understand both banking requirements and iGaming/fintech operational realities to build sustainable infrastructure.

Your payment orchestration platforms should integrate seamlessly with your business bank account, creating unified reporting and reconciliation. This integration eliminates manual data entry, reduces accounting errors, and provides real-time visibility into your financial position across all payment channels.

Choosing and managing your business bank account for fintech and iGaming success

Selecting the right business bank account for high-risk sectors requires evaluating factors beyond basic features. Start by assessing the bank's experience with iGaming and fintech clients. Banks unfamiliar with your industry often apply inappropriate risk frameworks that result in account freezes or closures. Ask potential banking providers about their high-risk client portfolio, average account longevity, and escalation procedures for unusual transaction patterns.

Your licensing and corporate structure must synchronize with your banking relationship. If you operate under a Curacao gaming license but bank in Europe, ensure your bank understands and accepts this arrangement. If your corporate entity is in BVI but you process payments through a UK subsidiary, document this structure clearly. Banks want to see coherent, compliant setups that minimize their regulatory exposure. Aligned structure and licensing improve bankability significantly.

Use this checklist when evaluating potential banking providers:

- Does the bank have documented experience serving iGaming or fintech clients in your operational jurisdictions?

- What transaction volume limits apply, and can they accommodate your projected growth over the next 12-24 months?

- How does the bank handle compliance reviews, and what documentation do they require for unusual transaction patterns?

- What integration options exist for connecting your bank account with payment processors, accounting software, and treasury management tools?

- What are the account maintenance fees, transaction fees, wire transfer costs, and foreign exchange spreads?

- Does the bank offer multi-currency accounts to minimize FX conversion costs for international transactions?

- What security features protect against fraud, including two-factor authentication, transaction limits, and real-time alerts?

Managing cash flow effectively requires connecting your business bank account with your payment processing infrastructure. Set up automated sweeps that move funds from your merchant account to your business bank account daily or weekly. This reduces the amount held in payment processor accounts and improves your control over working capital. Configure alerts for low balances, large transactions, and unusual activity patterns so you can respond quickly to potential issues.

Payment processing integration should enable automatic reconciliation between your payment gateway, merchant accounts, and business bank account. When a customer deposits $100, your system should automatically record the gross amount, processor fees, net settlement, and expected settlement date. This automation eliminates manual reconciliation work and ensures your financial records stay current. Many business bank account options offer APIs that facilitate this integration.

Compliance monitoring becomes simpler when you maintain clean separation between business and personal finances. Use your business bank account exclusively for business transactions. Never commingle personal expenses or transfers. This discipline protects you during audits, simplifies tax preparation, and maintains the legal separation between you and your business entity. It also makes your banking relationship more stable because banks can clearly see legitimate business activity without personal transaction noise.

Common pitfalls to avoid include underestimating transaction volume needs, neglecting to set up proper user permissions, and failing to maintain adequate reserves for rolling holds. Plan for growth by selecting accounts with transaction limits well above your current needs. Implement proper internal controls by giving team members only the access they need. Maintain reserves equal to at least one month of operating expenses plus any rolling reserves required by payment processors.

Pro Tip: Establish relationships with multiple banks in different jurisdictions before you need them. If your primary banking relationship encounters issues, having a backup account already open and operational prevents catastrophic business disruption.

Explore Deincepstart: your partner in banking and business solutions

Navigating the complex intersection of business banking and payment processing for iGaming and fintech requires specialized expertise. You need partners who understand both the technical requirements of high-risk payment processing and the relationship dynamics of securing stable banking.

Deincepstart offers comprehensive banking & business solutions tailored specifically for high-risk sectors. Our services include corporate bank account setup in banking-friendly jurisdictions, offshore structure optimization for operational efficiency, payment infrastructure design that integrates orchestration and open banking, and strategic advisory on maintaining long-term bankability. We help you build the financial foundation that supports sustainable growth in challenging regulatory environments.

FAQ

What is a high-risk merchant account, and why do iGaming businesses need one?

A high-risk merchant account is a specialized payment processing account designed for industries with elevated fraud and chargeback risks. iGaming businesses need these accounts because standard processors reject gaming transactions or terminate accounts upon discovering gaming activity. High-risk accounts include features like multi-PSP routing, cascading, and enhanced fraud filters that manage the unique challenges of gaming payments.

How does payment orchestration improve approval rates and reduce costs?

Payment orchestration routes transactions through multiple payment service providers based on intelligent algorithms that analyze transaction characteristics and provider performance. This increases approval rates by giving each payment multiple paths to success and reduces costs by automatically selecting the most cost-efficient routing for each transaction. The technology can boost approval rates by 20-25% while cutting processing costs significantly.

What features should fintech startups prioritize when selecting a business bank account?

Fintech startups should prioritize seamless integration with accounting and payment software, high transaction limits that accommodate rapid growth, and multi-user access with granular permission controls. Robust fraud protection, compliance support from banking relationship managers, and multi-currency capabilities for international operations are also essential. The bank's experience serving fintech clients and their willingness to grow with your business matters more than basic features.

Can open banking reduce transaction fees compared to traditional card payments?

Yes, open banking can reduce transaction fees by up to 50% compared to traditional card payments by eliminating card network intermediaries and interchange fees. Open banking connects directly to customer bank accounts through secure APIs, reducing per-transaction costs from 2.5-3.5% to 1.0-1.5%. It also enables real-time payouts that improve cash flow and customer satisfaction compared to the 3-5 day settlement times typical of card transactions.

Why is separating personal and business finances crucial for entrepreneurs?

Separating personal and business finances protects your personal assets from business liabilities by maintaining the legal distinction between you and your business entity. This separation simplifies accounting and tax reporting by creating clean records of business income and expenses. It also improves your banking relationships because banks can clearly identify legitimate business activity, and it provides better financial visibility for managing cash flow and making strategic decisions.