Securing a corporate bank account remains one of the toughest hurdles for fintech and iGaming entrepreneurs in 2026. Regulatory complexity has intensified across jurisdictions, with banks demanding robust compliance frameworks, capital reserves, and valid EMI or VASP licenses before approving accounts. Multi-jurisdictional requirements create confusion, delays stretch for months, and incomplete documentation triggers immediate rejections. This guide walks you through the exact prerequisites, application steps, and verification processes needed to streamline corporate account approval and maintain compliant banking relationships for your licensed business.

Table of Contents

- Understanding Prerequisites: Licenses, Capital, And Compliance Requirements

- Step-By-Step Process To Prepare And Submit Your Corporate Account Application

- Avoiding Pitfalls And Verifying Your Corporate Account Approval Success

- Comparing Corporate Account Setups: Offshore, Eu Anchor, And Multi-Jurisdictional Approaches

- Explore Tailored Banking And Business Solutions With Deincepstart

- Frequently Asked Questions About Corporate Account Approval

Key takeaways

| Point | Details |

|---|---|

| License and capital requirements | EMI licenses demand €350k+ initial capital and 3-4 month processing timelines in Lithuania with ~60% approval rates. |

| Compliance stack readiness | Proactive GRC, KYC, and transaction monitoring systems pass regulatory scrutiny and accelerate bank approval. |

| Multi-jurisdictional strategy | Combining offshore flexibility with EU anchor entities like Cyprus reduces laundering perception risks and improves banking access. |

| Document preparation | Complete entity structures, beneficial ownership declarations, and compliance certifications prevent the most common approval delays. |

| Ongoing verification | Regular account health checks and updated KYC documentation maintain approval status and prevent unexpected freezes. |

Understanding prerequisites: licenses, capital, and compliance requirements

Before submitting any corporate account application, you need the right licenses and compliance infrastructure in place. Banks assess your regulatory standing first, then evaluate your operational readiness.

EMI licenses require €350k+ initial capital with variable top-ups depending on transaction volumes. Lithuania processes applications in 3-4 months with approximately 60% approval rates, making it a competitive jurisdiction for fintech operators. Cyprus offers similar timelines but demands higher operational transparency and local presence requirements. Both jurisdictions require comprehensive business plans, risk management frameworks, and proof of technical infrastructure before granting licenses.

VASP licenses carry different demands. VASP regulations enforce AML travel rule compliance and know-your-transaction protocols across all crypto operations. Banking access varies significantly by jurisdiction, with Cyprus and Lithuania leading in VASP-friendly banking relationships. Estonia tightened requirements in 2024, making new VASP approvals rare. Malta maintains moderate accessibility but requires substantial local operational presence.

Capital requirements extend beyond initial licensing deposits. Banks expect 6-12 months of operational reserves, covering salaries, compliance costs, and transaction monitoring systems. Liquidity buffers demonstrate financial stability and reduce perceived default risk during account underwriting.

Compliance frameworks form the foundation of approval success. Anti-money laundering protocols must include customer due diligence, enhanced due diligence for high-risk clients, transaction monitoring with automated alerts, and suspicious activity reporting procedures. Know-your-customer systems need identity verification, address confirmation, beneficial ownership tracking, and ongoing customer screening against sanctions lists. The AML travel rule requires originator and beneficiary information for all crypto transfers above threshold amounts.

| License Type | Minimum Capital | Processing Time | Key Jurisdictions | Banking Access |

|---|---|---|---|---|

| EMI | €350k+ | 3-4 months | Lithuania, Cyprus | High |

| VASP | €125k+ | 4-6 months | Lithuania, Cyprus, Malta | Moderate |

| Payment Institution | €50k-€125k | 2-3 months | UK, Lithuania | High |

Pro Tip: Build your compliance stack before applying for licenses. Banks review your operational readiness during account applications, and a functioning GRC platform demonstrates maturity that accelerates approval timelines.

Deincepstart offers comprehensive banking and business solutions that align licensing strategy with banking infrastructure planning, ensuring your compliance foundation supports both regulatory approval and account access.

Step-by-step process to prepare and submit your corporate account application

Successful applications follow a systematic preparation sequence. Rushing submissions with incomplete documentation guarantees rejection and damages your banking reputation.

Step 1: Assemble your complete document package. Corporate account applications require certificate of incorporation, memorandum and articles of association, shareholder register with beneficial ownership declarations, director identification documents with proof of address, business plan with revenue projections, compliance manual covering AML and KYC procedures, and valid EMI or VASP license certificate. Missing any single document triggers immediate application suspension.

Step 2: Structure your entity correctly. Banks scrutinize corporate structures for complexity and risk indicators. Simple holding structures with transparent beneficial ownership receive faster approval than multi-layered offshore arrangements. Establish clear operational substance in your licensed jurisdiction through physical office space, local employees, and active business operations. Nominee directors raise red flags unless accompanied by substantial documentation explaining the arrangement.

Step 3: Deploy your compliance technology stack. A proactive compliance stack supports passing regulatory scrutiny consistently during bank reviews. Implement governance, risk, and compliance software for policy management and audit trails. Deploy automated KYC verification systems with document scanning and liveness detection. Install transaction monitoring platforms with configurable rule engines and case management workflows. Integrate sanctions screening that updates daily from OFAC, EU, and UN lists.

Step 4: Submit through proper channels. Most banks require relationship manager introductions rather than cold applications. Engage banking consultants with established bank relationships to facilitate warm introductions. Prepare a concise executive summary highlighting your license status, compliance readiness, and business model. Schedule preliminary calls to address bank concerns before formal submission.

Step 5: Navigate the review timeline. Initial screening takes 1-2 weeks as banks verify license validity and run preliminary compliance checks. Detailed due diligence extends 4-8 weeks, involving compliance team reviews, legal assessments, and risk committee approvals. Final approval and account setup require 2-3 weeks for documentation signing and system configuration. Total timelines range from 2-4 months for straightforward applications.

Common pitfalls derail applications even with complete documentation. Inconsistent beneficial ownership information across documents triggers fraud concerns. Vague business descriptions fail to demonstrate legitimate operations. Undercapitalized entities suggest financial instability. Incomplete compliance manuals indicate operational immaturity. Address these issues during preparation rather than during bank review.

Pro Tip: Test your compliance stack with mock transactions before submission. Banks increasingly request live demonstrations of your KYC and transaction monitoring capabilities during due diligence calls.

Leverage banking and business solutions to coordinate entity structuring, compliance deployment, and bank introductions as integrated services rather than fragmented efforts.

Avoiding pitfalls and verifying your corporate account approval success

Even approved accounts face ongoing scrutiny. Understanding common failure points and verification procedures protects your banking relationships.

Approval delays stem from predictable mistakes. Incomplete beneficial ownership declarations cause 40% of application suspensions. Banks demand full ownership chains traced to natural persons, not stopping at intermediate holding companies. Outdated compliance manuals lacking current AML regulations signal operational neglect. Insufficient operational substance in licensed jurisdictions raises shell company concerns. Weak transaction monitoring capabilities fail to demonstrate risk management maturity.

Offshore structures carry laundering perception risks despite legitimate business purposes. Banks increasingly view pure offshore arrangements as high-risk, demanding enhanced due diligence and imposing transaction limits. Balanced multi-jurisdictional setups combining offshore flexibility with EU anchor entities reduce perceived risks and improve banking access. Cyprus-based operational entities paired with BVI holding structures demonstrate legitimate tax planning while maintaining regulatory credibility.

Verifying account approval status requires active confirmation beyond initial setup. Request written confirmation of account activation with specified transaction limits and currency capabilities. Test small transactions across all intended payment corridors before launching full operations. Confirm correspondent banking relationships for international transfers, as some accounts approve domestic operations only. Review monthly account statements for unexpected restrictions or holds.

Preventing account freezes demands ongoing compliance diligence. Update KYC documentation annually for all directors and beneficial owners. Submit quarterly transaction reports demonstrating business activity patterns. Respond immediately to bank information requests, as delayed responses trigger automatic account reviews. Maintain capital buffers above minimum requirements to avoid liquidity concerns.

Best practices for account health include regular compliance audits by external firms, proactive communication with relationship managers about business changes, immediate reporting of suspicious activity detected in your monitoring systems, and maintaining separate accounts for operational funds versus client money.

Warning: A single compliance failure can terminate banking relationships across multiple institutions. Banks share information through industry networks, and reputational damage spreads quickly. Invest in compliance infrastructure as operational insurance, not regulatory burden.

Deincepstart provides banking and business solutions that include ongoing compliance monitoring and relationship management, ensuring your accounts remain active and healthy beyond initial approval.

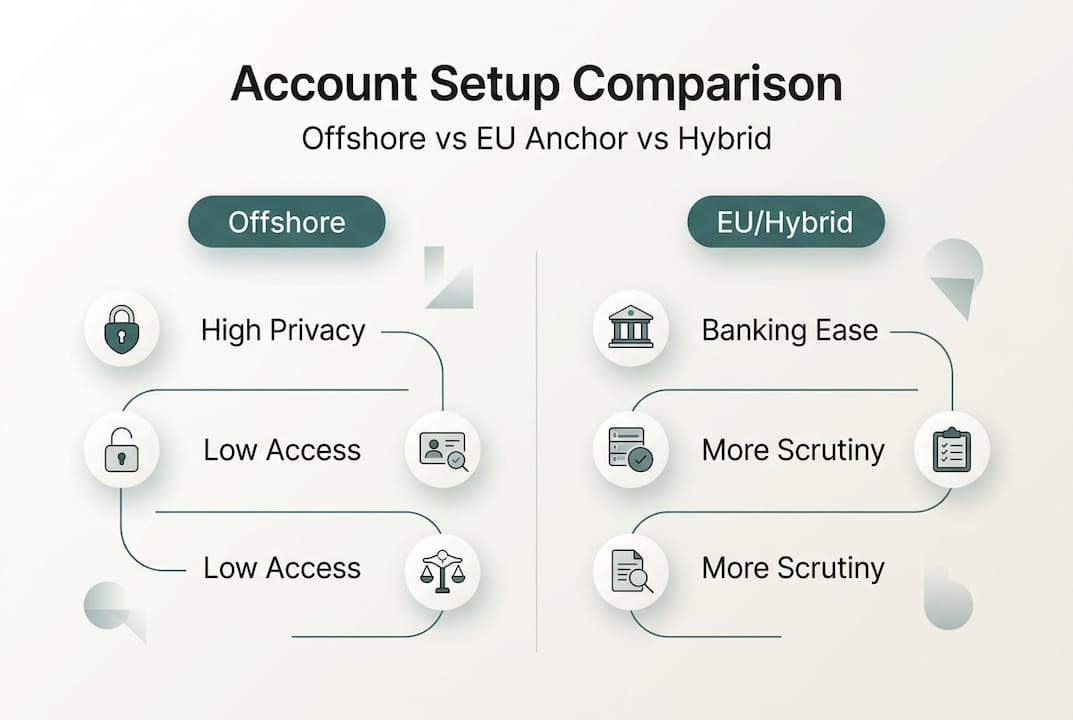

Comparing corporate account setups: offshore, EU anchor, and multi-jurisdictional approaches

Strategic structure selection impacts approval probability and operational flexibility. Each approach carries distinct trade-offs for fintech and iGaming operators.

Offshore-only structures maximize tax efficiency and operational privacy. BVI, Cayman, Nevis, Seychelles, and Mauritius offer zero corporate tax, minimal reporting requirements, and confidential beneficial ownership registers. However, multi-jurisdictional setups with EU anchors balance compliance better than offshore-only arrangements. Banks increasingly reject pure offshore applications due to FATF pressure and money laundering concerns.

EU anchor structures establish operational credibility through licensed entities in Lithuania, Cyprus, or Malta. These jurisdictions provide regulatory legitimacy while maintaining competitive tax rates through IP box regimes and holding company exemptions. EU entities access SEPA payment networks and correspondent banking relationships unavailable to offshore companies. Compliance costs increase due to local audit requirements and regulatory reporting obligations.

Hybrid multi-jurisdictional approaches combine offshore holding companies with EU operational entities. This structure preserves tax efficiency at the holding level while demonstrating regulatory compliance through licensed operations. Dividend flows from EU subsidiaries to offshore parents benefit from participation exemptions and double tax treaties. Banking relationships focus on the EU entity, reducing offshore perception risks.

| Structure Type | Banking Access | Compliance Cost | Tax Efficiency | Regulatory Scrutiny | Best For |

|---|---|---|---|---|---|

| Offshore-only | Low | Low | Highest | Highest | Established operators with existing banking |

| EU anchor | High | High | Moderate | Low | New EMI/VASP license holders |

| Multi-jurisdictional | High | Moderate | High | Moderate | Scaling fintech and iGaming businesses |

EMI and VASP license holders benefit most from EU anchor or multi-jurisdictional setups. Licensing authorities expect operational substance in the jurisdiction of authorization, making pure offshore structures incompatible with license maintenance requirements. Cyprus and Lithuania explicitly require licensed entities to maintain local offices, staff, and management presence.

iGaming operators face additional considerations. Payment processing demands robust correspondent banking networks that offshore structures cannot access. Multi-jurisdictional setups enable diversified payment routing through different entities, reducing single point of failure risks. Regulatory changes in one jurisdiction become manageable when operations span multiple legal entities.

Key selection factors include current banking relationships, target markets and their regulatory requirements, transaction volumes and currency needs, compliance team capabilities, and growth timeline and scaling plans.

Deincepstart specializes in banking and business solutions tailored to your specific operational model, designing multi-jurisdictional structures that optimize banking access, compliance costs, and tax efficiency simultaneously.

Explore tailored banking and business solutions with Deincepstart

Navigating corporate account approval demands expertise across licensing, compliance, and banking relationships. Deincepstart Ltd brings specialized knowledge in fintech and iGaming corporate banking, helping you secure accounts that support your business operations from day one.

Our corporate banking and business solutions cover complete account setup processes, from entity structuring through final approval. We provide EMI and VASP licensing guidance, compliance stack implementation, bank relationship introductions, and ongoing account management. Our Hong Kong base and global network enable us to design multi-jurisdictional structures that balance offshore flexibility with EU regulatory credibility.

We understand the unique challenges iGaming operators and crypto businesses face in banking access. Our services include tax residency planning, dividend structuring, and cross-border payment transit solutions specifically designed for high-risk industries. Whether you need BVI holding structures, Cyprus operational entities, or Lithuanian EMI licenses, we coordinate every element to ensure your corporate banking infrastructure supports sustainable growth.

Visit our site to explore how expert fintech compliance support can streamline your path to corporate account approval and operational success in 2026.

Frequently asked questions about corporate account approval

Can I open a corporate account without an EMI or VASP license?

Traditional corporate accounts remain available without specialized licenses for standard business operations. However, fintech payment processing and crypto exchange activities require EMI or VASP licenses before any reputable bank will approve accounts. Banks immediately reject applications from unlicensed entities conducting regulated financial services.

How long does corporate account approval typically take in Lithuania?

Lithuanian banks process corporate account applications in 2-4 months for licensed EMI and VASP entities with complete documentation. Initial screening completes within 2 weeks, detailed due diligence extends 6-10 weeks, and final approval with account setup requires 2-3 weeks. Incomplete applications or complex ownership structures extend timelines by 4-8 weeks.

What documents most commonly cause delays in approval?

Beneficial ownership declarations cause the majority of delays when ownership chains remain incomplete or inconsistent across documents. Compliance manuals lacking current AML regulations signal operational immaturity. Outdated director identification documents or proof of address older than 3 months trigger automatic requests for updated materials. Business plans without detailed revenue projections and market analysis fail to demonstrate operational viability.

Is a multi-jurisdictional setup always safer than offshore-only?

Multi-jurisdictional structures with EU anchors consistently receive better banking treatment than pure offshore arrangements in 2026. However, complexity increases compliance costs and management overhead. Established businesses with existing banking relationships may maintain offshore-only structures successfully. New EMI and VASP license holders require EU operational presence to satisfy licensing authorities and secure initial banking relationships.

What ongoing compliance is required after approval?

Approved accounts demand annual KYC updates for all directors and beneficial owners, quarterly transaction reports demonstrating normal business patterns, immediate responses to bank information requests, and maintenance of capital reserves above minimum license requirements. External compliance audits every 12-18 months demonstrate ongoing operational maturity. Failure to maintain these standards triggers account reviews and potential suspension.