Hong Kong processes over $1.3 trillion in cross-border payments annually, making it one of the world's busiest financial hubs for international transactions. For iGaming operators and fintech entrepreneurs, this massive payment infrastructure translates into practical advantages: seamless multi-currency operations, robust regulatory frameworks, and direct access to Mainland China markets through preferential trade agreements. Opening a corporate bank account in Hong Kong isn't just about prestige. It's about leveraging a financial ecosystem specifically built for cross-border commerce, equipped with cutting-edge RegTech compliance tools, and supported by over 1,100 fintech companies that understand your industry's unique challenges.

Table of Contents

- Key takeaways

- Hong Kong's strategic role in cross-border banking for fintech and iGaming

- Robust fintech ecosystem and regulatory compliance in Hong Kong

- Practical considerations and step-by-step guide to opening your Hong Kong bank account

- Comparing Hong Kong banking options for fintech and iGaming operators

- Discover tailored banking and business solutions with Deincepstart

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Offshore RMB hub | Hong Kong processes RMB transactions outside Mainland China, enabling currency flexibility and reducing conversion frictions for cross-border payments. |

| Multi currency accounts | Accounts can hold and settle USD, EUR, CNY, HKD and RMB, consolidating regional banking needs into a single platform. |

| CEPA access | CEPA agreements provide preferential market access and faster settlements for financial services between Hong Kong and Mainland China. |

| Real time settlement | The strategic location enables real time settlement during Asian business hours, improving cash flow for cross-border operations. |

Hong Kong's strategic role in cross-border banking for fintech and iGaming

Hong Kong's position as a strategic gateway to Mainland China fundamentally changes how iGaming and fintech operators handle cross-border payments. The Closer Economic Partnership Arrangement (CEPA) creates preferential terms for financial services, reducing barriers that typically complicate international transactions. This isn't theoretical policy. It translates into faster settlement times, lower conversion costs, and simplified regulatory pathways when moving funds between Hong Kong and Mainland markets.

As the world's largest offshore RMB hub, Hong Kong handles RMB transactions outside Mainland China's strict capital controls. For fintech platforms processing payments from Chinese customers or iGaming operators managing player deposits in multiple currencies, this capability eliminates conversion chains that eat into margins. You can hold, transfer, and settle RMB transactions with the same ease as USD or EUR, all within accounts that support five major currencies simultaneously.

The multi-currency account structure solves a persistent headache for cross-border businesses: maintaining separate banking relationships in different jurisdictions. Instead of juggling accounts in the US for USD, Europe for EUR, and Asia for CNY, you consolidate operations into Hong Kong accounts that natively support all three plus HKD and RMB. This consolidation reduces administrative overhead, simplifies reconciliation, and provides clearer visibility into cash positions across your global operations.

Key advantages of Hong Kong's banking ecosystem for your business:

- CEPA agreements provide preferential market access and reduced compliance complexity for Mainland transactions

- Multi-currency capabilities eliminate the need for multiple regional banking relationships

- Offshore RMB operations bypass Mainland capital controls while maintaining currency flexibility

- Geographic positioning enables real-time settlement during Asian business hours

- Established financial infrastructure reduces operational risks compared to emerging fintech hubs

These structural advantages create compounding benefits. Lower transaction costs improve margins. Faster settlement enhances cash flow. Simplified compliance reduces legal overhead. For businesses operating in regulated industries like iGaming, where banking relationships often prove challenging, Hong Kong's mature ecosystem offers stability that newer fintech jurisdictions can't match.

Robust fintech ecosystem and regulatory compliance in Hong Kong

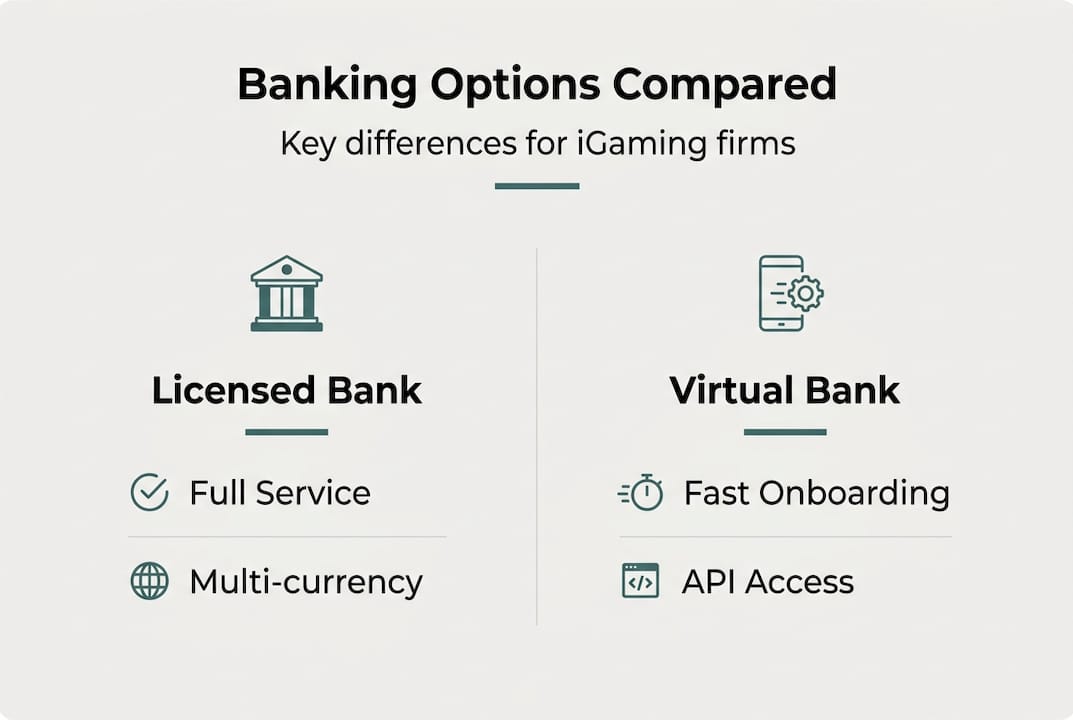

Hong Kong's fintech landscape operates at a scale that supports serious commercial operations, not experimental ventures. With over 1,100 fintech companies, 150+ licensed banks, 8 virtual banks, and 120+ digital payment firms, you're entering an ecosystem where financial infrastructure providers compete for your business rather than treating you as a compliance risk to be managed.

The presence of eight virtual banks fundamentally changed account opening dynamics. These digital-first institutions process applications faster than traditional banks, often completing onboarding in two to three weeks versus the six to eight weeks typical of legacy institutions. They've built their systems around API integrations, automated compliance checks, and digital KYC processes that align naturally with fintech and iGaming business models. You're not forcing your digital business into analog banking processes.

| Institution Type | Count | Primary Advantage | Typical Onboarding |

|---|---|---|---|

| Licensed Banks | 150+ | Comprehensive services, established reputation | 6-8 weeks |

| Virtual Banks | 8 | Fast digital onboarding, API-first architecture | 2-3 weeks |

| Digital Payment Firms | 120+ | Specialized payment solutions, platform integrations | 3-4 weeks |

| Fintech Companies | 1,100+ | Innovative products, niche service focus | Varies |

RegTech adoption rates of 95-97% among Hong Kong banks mean compliance processes that once required weeks of manual review now complete in days through automated systems. These platforms cross-reference your business against sanctions lists, verify beneficial ownership structures, and assess transaction patterns using the same technology that powers the compliance departments of global financial institutions. The result: fewer delays from manual review backlogs and more consistent application of compliance standards.

Pro Tip: Select banks with demonstrated RegTech integration rather than those still relying on manual compliance reviews. Ask potential banking partners about their automated KYC systems and average processing times for fintech or iGaming applications. Banks using advanced compliance automation can reduce your onboarding timeline by 40-60%.

The concentration of digital payment firms creates practical advantages beyond basic banking. These specialized providers offer payment gateway integrations, fraud detection systems, and settlement optimization tools built specifically for online platforms. For iGaming operators managing thousands of daily transactions across multiple currencies, partnering with Hong Kong payment firms means accessing infrastructure designed for your transaction volumes and risk profiles.

This ecosystem density creates network effects. Banks understand fintech business models because they work with hundreds of similar companies. Payment processors have solved integration challenges you'll face because they've onboarded dozens of iGaming platforms. Compliance consultants know exactly which documentation satisfies regulators because they've guided countless applications through approval. You benefit from accumulated institutional knowledge rather than educating each service provider about your industry.

Practical considerations and step-by-step guide to opening your Hong Kong bank account

Successful bank account opening in Hong Kong follows a predictable sequence, but preparation determines whether you complete the process in weeks or months. The banks and regulators aren't obstacles to navigate but partners evaluating whether your business fits their risk appetite and compliance frameworks. Approaching the process with this mindset changes how you prepare documentation and respond to inquiries.

-

Prepare comprehensive corporate documentation including certificate of incorporation, articles of association, shareholder registry, and beneficial ownership declarations for all parties holding 10% or greater stakes in your company.

-

Choose your banking partner based on your specific business model, whether traditional licensed banks for comprehensive services and established relationships, virtual banks for speed and digital integration, or specialized payment firms for transaction processing capabilities.

-

Submit your application with complete due diligence packages including detailed business plans, projected transaction volumes by currency, source of funds documentation, and industry-specific compliance materials such as gaming licenses or payment processor registrations.

-

Complete identity verification through in-person interviews at Hong Kong branches or video KYC sessions for remote applications, ensuring all beneficial owners and authorized signatories participate in verification processes.

-

Respond promptly to follow-up requests for additional documentation or clarification, treating each inquiry as an opportunity to demonstrate your business's legitimacy and compliance readiness rather than viewing questions as obstacles.

Pro Tip: iGaming operators should proactively address compliance concerns by including copies of gaming licenses, responsible gambling policies, and AML procedures in initial applications. Banks appreciate transparency about industry risks and respond more favorably when you demonstrate awareness of compliance requirements upfront rather than treating them as afterthoughts.

The documentation requirements reflect banks' need to satisfy Hong Kong Monetary Authority oversight and international AML standards. For fintech and iGaming businesses, this means going beyond basic corporate paperwork to demonstrate operational legitimacy. Include evidence of actual business activities: customer agreements, platform screenshots, transaction processing records, and regulatory correspondence from jurisdictions where you operate.

Common misconceptions about account denial due to iGaming sector involvement often stem from incomplete applications rather than blanket industry exclusions. Hong Kong banks work with regulated gaming operators regularly. They decline applications lacking proper licensing, unclear beneficial ownership, or insufficient AML controls. The distinction matters. A licensed iGaming operator with transparent ownership and robust compliance documentation presents manageable risk. An unlicensed operation with opaque ownership and minimal controls doesn't.

Timeline expectations should account for complexity. A straightforward fintech application with clean documentation might clear in three weeks through a virtual bank. An iGaming operator with multi-jurisdictional licensing and complex ownership structures could require two months even with perfect paperwork. Build buffer time into your planning rather than assuming best-case scenarios.

Comparing Hong Kong banking options for fintech and iGaming operators

Selecting the right banking partner requires matching institutional capabilities to your operational needs. The Hong Kong fintech ecosystem offers distinct options, each with tradeoffs in cost, speed, features, and compliance approaches. Understanding these differences prevents mismatched expectations and costly switches after onboarding.

| Bank Type | Setup Time | Currency Options | Monthly Fees | Compliance Approach | API Integration |

|---|---|---|---|---|---|

| Licensed Banks | 6-8 weeks | 15-25 currencies | $200-500 | Manual + automated review | Limited, legacy systems |

| Virtual Banks | 2-3 weeks | 8-12 currencies | $50-150 | Automated RegTech | Native API, modern stack |

| Payment Firms | 3-4 weeks | 10-15 currencies | $100-300 | Specialized risk models | Extensive payment APIs |

Licensed banks bring institutional weight and comprehensive service offerings. They handle complex treasury needs, provide trade finance facilities, and maintain correspondent banking relationships that facilitate transactions in exotic currencies. The tradeoff: slower processes, higher fees, and integration challenges with modern tech stacks. Choose licensed banks when you need sophisticated financial services beyond basic accounts or when counterparties require the credibility of established banking relationships.

Virtual banks optimize for speed and digital integration. Their cloud-native platforms expose APIs for balance queries, transaction initiation, and webhook notifications that integrate cleanly with modern fintech architectures. Compliance automation means faster decisions but sometimes less flexibility for edge cases. Virtual banks work well for digitally native businesses with straightforward compliance profiles and strong technical capabilities to leverage API integrations.

Payment firms specialize in transaction processing rather than full banking services. They excel at high-volume, low-value transactions with built-in fraud detection and currency optimization. Many offer specialized features for iGaming like player wallet management, responsible gambling controls, and jurisdiction-specific compliance tools. Consider payment firms as complements to traditional banking rather than replacements, handling transaction flow while banks manage treasury and corporate finance needs.

Key factors when evaluating banking partners:

- Transaction volume capacity and per-transaction fees that align with your business model

- Multi-currency support for specific currencies your business requires, not just generic offerings

- Compliance expertise with your specific industry, demonstrated through existing client relationships

- Technical integration capabilities matching your platform architecture and development resources

- Relationship management approach, whether you need dedicated account managers or prefer self-service portals

The optimal strategy for many fintech and iGaming operators combines multiple relationships. Use a licensed bank for corporate treasury and regulatory credibility. Add a virtual bank for operational accounts and digital integration. Partner with specialized payment firms for transaction processing. This multi-provider approach builds redundancy, optimizes costs across different transaction types, and prevents single points of failure in your financial infrastructure.

Cost structures vary significantly beyond headline monthly fees. Licensed banks may charge $400 monthly but include services that virtual banks bill separately. Payment firms might advertise low base fees but apply percentage charges on transaction volumes that dwarf fixed costs at scale. Model total costs across realistic transaction scenarios rather than comparing fee schedules in isolation.

Discover tailored banking and business solutions with Deincepstart

Navigating Hong Kong's banking landscape becomes significantly simpler when you work with advisors who understand both the financial infrastructure and your industry's specific challenges. Deincepstart specializes in helping iGaming operators and fintech companies establish corporate bank accounts and build compliant payment systems in Hong Kong. We've guided dozens of businesses through the account opening process, leveraging relationships with licensed banks, virtual banks, and payment providers to match you with institutions aligned to your business model.

Our services extend beyond basic account opening to comprehensive financial infrastructure planning. We help structure offshore entities in BVI, Cayman, Nevis, Seychelles, and Mauritius that optimize tax efficiency while satisfying Hong Kong banks' due diligence requirements. For businesses requiring specialized licenses, we facilitate EMI and VASP applications, ensuring your regulatory foundation supports sustainable growth. Our cross-border payment transit solutions address the unique challenges iGaming and fintech businesses face when traditional banking relationships prove difficult.

Explore how Deincepstart's banking and business solutions can streamline your Hong Kong account setup and build the compliant financial infrastructure your business needs to scale across borders.

Frequently asked questions

What documents do iGaming and fintech companies need to open a Hong Kong bank account?

You'll need standard corporate documents including certificate of incorporation, articles of association, shareholder registry, and beneficial ownership declarations for stakeholders holding 10% or greater equity. iGaming operators must additionally provide gaming licenses from operating jurisdictions, AML policies, and responsible gambling procedures. Fintech companies should include payment processor registrations, regulatory approvals from home jurisdictions, and detailed business plans explaining revenue models and transaction flows. Banks increasingly request projected transaction volumes by currency and source of funds documentation for initial capitalization.

How long does the bank account opening process take in Hong Kong?

Typical timelines range from two to eight weeks depending on bank type and application complexity. Virtual banks process straightforward fintech applications in two to three weeks using automated compliance systems. Licensed banks require six to eight weeks for thorough manual review processes. iGaming operators should expect longer timelines regardless of bank type due to enhanced due diligence requirements. Incomplete documentation or unclear beneficial ownership structures can extend timelines by several weeks as banks request additional information.

Can iGaming operators face challenges opening bank accounts in Hong Kong?

Yes, iGaming operators encounter heightened scrutiny due to AML regulations and perceived industry risks, but these challenges are manageable with proper preparation. Banks primarily decline applications lacking valid gaming licenses, transparent ownership structures, or robust compliance controls rather than rejecting the industry categorically. Hong Kong's mature fintech environment includes banks and payment firms experienced with regulated gaming operators. Working with advisors who understand both banking requirements and iGaming compliance significantly improves approval rates and reduces processing delays.

What multi-currency options are available with Hong Kong bank accounts?

Hong Kong bank accounts commonly support USD, HKD, EUR, CNY, and RMB within single multi-currency account structures, eliminating the need for separate accounts in different jurisdictions. As the world's largest offshore RMB hub, Hong Kong enables RMB transactions outside Mainland China's capital controls. Licensed banks typically offer 15 to 25 currency options including exotic currencies for specialized trade needs. Virtual banks focus on eight to twelve major currencies optimized for digital businesses. This multi-currency capability streamlines cross-border payments, reduces conversion costs, and simplifies treasury management for businesses operating across multiple markets.