Most iGaming operators and fintech founders assume corporate banking is just a bigger version of a business checking account. It is not. Corporate banking is a distinct financial segment built for scale, complexity, and customization that retail and commercial banking simply cannot match. Global revenues exceeded $1.5 trillion, representing 28% of all financial intermediation revenues worldwide. If you are building a cross-border payments platform or running a licensed iGaming operation, understanding this segment is not optional. It is the foundation of your financial infrastructure.

Table of Contents

- What is corporate banking?

- Corporate banking vs. other banking segments

- Core services in corporate banking

- How fintech disrupts and enables corporate banking

- Common pitfalls and key compliance considerations

- Strategic applications: Choosing and using corporate banking solutions

- Explore tailored banking and compliance solutions

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Corporate banking scope | It serves mid-size and large organizations with customized, large-scale financial solutions. |

| Fintech and BaaS role | Fintech platforms offer faster onboarding but come with greater regulatory scrutiny, especially for high-risk sectors. |

| Essential services | Lending, treasury management, and trade finance are core services central to corporate banking value. |

| Compliance complexity | Rigorous due diligence and KYC requirements make preparation critical for fintech and iGaming firms. |

| Strategic selection | Choosing the right blend of banking solutions depends on company needs, appetite for speed, and risk profile. |

What is corporate banking?

Corporate banking is a specialized division within financial institutions that serves mid-size firms, large corporations, and multinational enterprises. It is not the same as commercial banking, which targets small and medium-sized businesses (SMEs), and it is nothing like retail banking, which serves individual consumers.

The core distinction is customization. Corporate banking delivers tailored solutions including lending, treasury management, risk management, trade finance, and cash management to organizations with complex, high-volume financial needs. You get a dedicated relationship manager, not a call center. You negotiate terms, not accept defaults.

Here is a quick look at what corporate banking actually covers:

- Lending and credit facilities: Revolving credit lines, syndicated loans, and asset-based lending

- Treasury and cash management: Liquidity optimization, multi-currency accounts, and cash pooling

- Trade finance: Letters of credit, guarantees, and supply chain financing

- Risk management: Hedging instruments, FX risk tools, and interest rate swaps

- Payment infrastructure: Cross-border wire transfers, SWIFT access, and settlement accounts

"Corporate banking is not a product. It is a relationship built around your business model, your risk profile, and your growth trajectory."

For iGaming operators seeking corporate bank account approval, understanding this relationship-driven model is the first step toward getting the right banking partner in place.

Corporate banking vs. other banking segments

To understand where corporate banking fits, you need to see how it compares to the alternatives. The differences are not just cosmetic. They affect loan sizes, onboarding timelines, compliance requirements, and the level of service you receive.

| Feature | Corporate banking | Commercial banking | Retail banking |

|---|---|---|---|

| Client type | Large corps, multinationals | SMEs, local businesses | Individuals |

| Loan size | $2M to over $1B | $50K to $2M | Under $50K |

| Onboarding time | 3 to 6 months | 2 to 8 weeks | Days |

| Customization | Fully bespoke | Moderate | Standardized |

| Compliance depth | Extensive KYC/AML | Standard | Basic |

| Relationship model | Dedicated manager | Branch or online | Self-service |

Asset-based loans range from $2M to over $1B in corporate banking, with dedicated relationship managers handling complex, multi-jurisdictional needs. That scale is simply not available through commercial or retail channels.

For fintech startups and iGaming operators, the onboarding complexity is the biggest shock. If you walk into a corporate bank without the right documentation, structure, and compliance history, you will wait months and likely get rejected. Getting your corporate bank account setup right from the start saves you that pain.

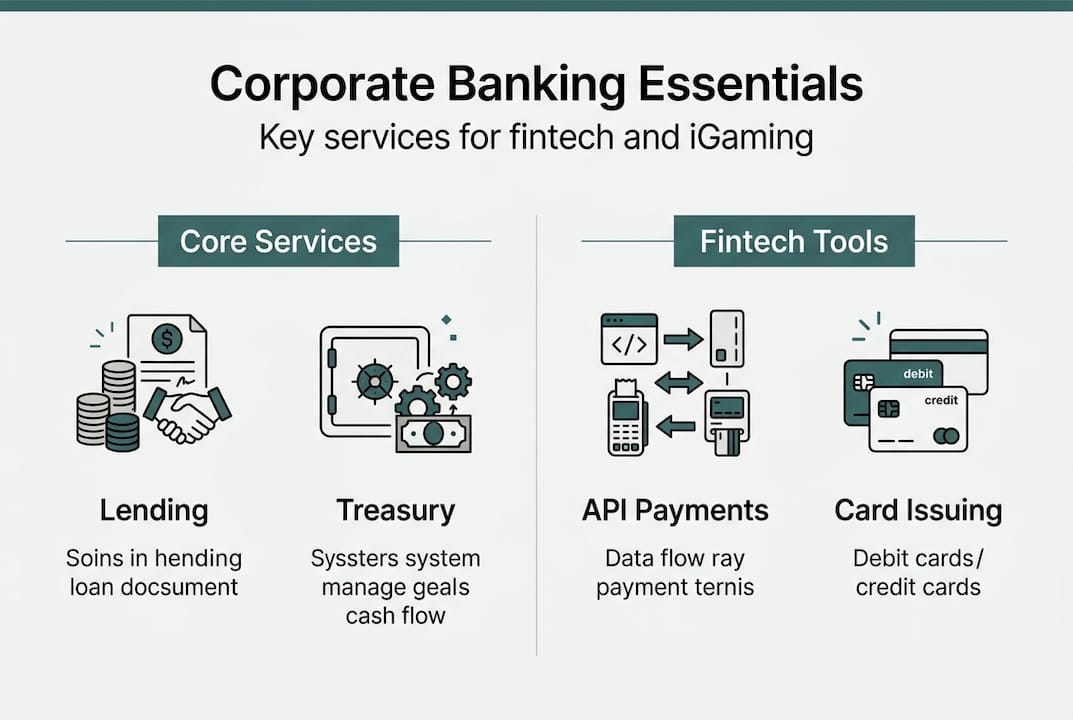

Core services in corporate banking

Once you know the types of banking, the concrete services become much clearer. Here is how each core service maps to real operational needs for iGaming and fintech businesses:

- Lending and credit lines: Revolving facilities let you manage cash flow during peak player acquisition periods without liquidating assets. Syndicated loans fund major platform builds or acquisitions.

- Treasury and cash management: Multi-currency pooling lets you consolidate balances across jurisdictions, reduce FX conversion costs, and optimize liquidity in real time.

- Risk management: FX hedging protects your margins when you operate in multiple currencies. Interest rate swaps stabilize borrowing costs on long-term facilities.

- Trade finance: Letters of credit and bank guarantees support vendor relationships and licensing requirements in regulated markets.

- Cross-border payments: SWIFT-enabled accounts and correspondent banking relationships let you move funds between jurisdictions with speed and auditability.

Corporate banking delivers customized solutions across all these categories, but the relationship manager is the glue. They advocate for your account internally, escalate compliance reviews, and help you structure transactions correctly.

Pro Tip: The service that trips up most new iGaming and fintech clients is treasury management. Operators underestimate how many currencies, payment processors, and settlement accounts they will need to manage simultaneously. Build your treasury structure before you need it, not after.

If your current provider lacks the tools you need, reviewing risk management service alternatives can help you identify better-fit partners.

How fintech disrupts and enables corporate banking

Banking-as-a-Service (BaaS) platforms have fundamentally changed who can access corporate-grade banking infrastructure. BaaS is a model where licensed banks expose their core banking functions through APIs, allowing fintech companies to embed those services into their own platforms without holding a full banking license.

BaaS platforms enable API-driven payments, card issuing, and for-benefit-of (FBO) accounts, giving fintech operators scalable corporate banking capabilities in weeks rather than months.

Here is how the two paths compare:

| Factor | Traditional corporate bank | BaaS or fintech platform |

|---|---|---|

| Onboarding time | 3 to 6 months | 2 to 8 weeks |

| Fees | Lower long-term | Higher per-transaction |

| Compliance support | Extensive internal teams | Varies by provider |

| High-risk sector access | Often restricted | More flexible |

| Customization | Deep, relationship-driven | API-configurable |

- Traditional banks offer lower fees and deeper compliance infrastructure but move slowly and often reject high-risk sectors outright.

- BaaS platforms offer speed and flexibility but come with higher per-transaction costs and variable regulatory certainty.

- Offshore banking structures can bridge the gap for operators who need both speed and jurisdictional flexibility.

Pro Tip: If your business is in iGaming, crypto, or high-risk fintech, do not start with a tier-one bank. Use a BaaS or offshore solution to build your transaction history and compliance record first. Then approach traditional corporate banks from a position of strength.

For deeper context on navigating this decision, fintech banking compliance insights and iGaming fintech payments are worth reviewing before you commit to a provider.

Common pitfalls and key compliance considerations

Fintech options are appealing, but compliance missteps are common. Here is what you should watch out for:

- Incomplete KYC documentation: Missing UBO (ultimate beneficial owner) declarations, outdated corporate registrations, or unverified source-of-funds documentation will stall or kill your application.

- Misclassified business activity: Describing your iGaming operation as a generic "software company" triggers enhanced due diligence and damages trust with the bank.

- Ignoring AML policy alignment: Your internal AML program must match the bank's standards. If you cannot demonstrate a functioning compliance framework, expect rejection.

- Underestimating onboarding timelines: High-risk sectors face weeks-to-months delays compared to standard corporate clients, with higher fees and more scrutiny at every stage.

- Choosing the wrong jurisdiction: Opening accounts in jurisdictions that conflict with your licensing or player base creates regulatory exposure.

"The biggest mistake operators make is treating banking as an afterthought. By the time they need the account, they have no time to do it properly."

Pro Tip: Prepare a banking memorandum before you approach any institution. This document summarizes your business model, revenue sources, compliance framework, and corporate structure. It signals professionalism and dramatically reduces back-and-forth during due diligence.

Reviewing fintech licensing examples for high-risk startups gives you a clearer picture of what compliance documentation banks actually expect.

Strategic applications: Choosing and using corporate banking solutions

Knowing the pitfalls, here is how to approach your own corporate banking choices with a clear framework.

- Assess your risk profile: Are you in a regulated iGaming market, a crypto-adjacent fintech, or a cross-border payments business? Your risk classification determines which banks will even consider you.

- Map your transaction flows: Identify every currency, jurisdiction, and payment method you need to support. This shapes your account structure and treasury requirements.

- Choose your structure first: Offshore entities in BVI, Cayman, or Seychelles can unlock banking relationships that are unavailable to onshore companies in high-risk sectors.

- Build your compliance record: Use BaaS or EMI accounts to generate clean transaction history before approaching tier-one corporate banks.

- Engage a relationship manager early: Do not submit cold applications. Get an introduction through an advisor or existing banking relationship.

Corporate banking emphasizes relationship-driven, customized services for global enterprises, with a value chain that runs from funding acquisition through credit assessment, lending, and risk management. That chain only works when you enter it at the right point.

| Scenario | Recommended solution |

|---|---|

| New iGaming operator, no banking history | BaaS or EMI account, offshore structure |

| Established fintech, scaling cross-border | Traditional corporate bank with BaaS overlay |

| Crypto business needing fiat rails | Offshore bank plus VASP-licensed EMI |

| iGaming operator in regulated EU market | Tier-two EU bank with dedicated compliance team |

For operators considering banking offshore for iGaming, Hong Kong remains one of the most strategically positioned jurisdictions for cross-border financial infrastructure in 2026.

Explore tailored banking and compliance solutions

If this article clarified the complexity of corporate banking for your operation, the next step is getting the right structure in place before you need it. Most operators who come to us have already lost months to rejected applications or misaligned banking partners.

At Deincepstart Ltd, we specialize in helping iGaming operators, fintech companies, and crypto businesses navigate exactly this process. From offshore entity formation in BVI, Cayman, and Seychelles to EMI licensing, VASP registration, and corporate account placement, we build the financial infrastructure your business actually needs. If you are ready to move faster and smarter, explore Deincepstart banking and business solutions and connect with our advisory team today.

Frequently asked questions

What makes corporate banking different from commercial banking?

Corporate banking delivers customized solutions for large corporations including bespoke lending, treasury management, and trade finance, while commercial banking serves smaller businesses with more standardized, off-the-shelf products.

Do fintech platforms offer true corporate banking?

Fintechs deliver many core corporate banking services through API-driven BaaS platforms including payments, card issuing, and FBO accounts, but they may not provide the full regulatory certainty or fee structures of a licensed corporate bank.

How long does it take to open a corporate bank account?

Traditional corporate bank onboarding typically takes 3 to 6 months. High-risk sectors face weeks-to-months timelines with BaaS alternatives, but with higher fees and more scrutiny throughout the process.

What are examples of core corporate banking services for iGaming?

Corporate banking provides customized solutions including asset-based lending, global treasury management, cross-border payment infrastructure, and compliance-aligned account structures specifically suited to high-risk operators.