Payment processing in iGaming is not the same game as mainstream e-commerce. Decline rates exceed 13%, which is roughly three times higher than standard online retail. That single statistic tells you everything about why operators and fintech founders need a fundamentally different approach to building their financial infrastructure. This guide breaks down the core mechanics, the high-risk realities, the best payment methods, compliance obligations, and how to build a stack that actually holds up under regulatory and operational pressure.

Table of Contents

- Understanding payment processing: Core components and workflows

- Why iGaming and fintech payment processing is considered high-risk

- Payment methods compared: Cards, open banking, and crypto

- Key compliance standards: KYC, AML, and regulatory frameworks

- Building a resilient payment infrastructure for iGaming and fintech

- Partnering for success: How Deincepstart can help

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Payment flow complexity | iGaming and fintech payments face unique risks, costs, and compliance hurdles not found in standard e-commerce. |

| Method selection matters | Blending payment options like open banking and crypto can lower costs and reduce chargebacks. |

| Ongoing compliance is key | Staying ahead of regulations like MiCA is essential to avoid penalties and bank disruptions. |

| Orchestration boosts revenue | Using multiple PSPs and payment rails optimizes approval rates and player lifetime value. |

Understanding payment processing: Core components and workflows

Payment processing is the end-to-end system that moves money from a player or customer to your business account. It involves four main players: the merchant (you, the operator), the acquirer (the bank that processes on your behalf), the issuer (the player's bank or card provider), and the PSP (payment service provider, which connects all parties and manages the technical layer).

Here is how a typical transaction flows:

- A player initiates a deposit.

- The PSP sends an authorization request to the acquirer.

- The acquirer forwards it to the card network (Visa, Mastercard) or payment rail.

- The issuer approves or declines based on risk and balance checks.

- The result returns through the same chain in seconds.

- Clearing and settlement follow, usually within one to three business days.

Approval rates vary significantly depending on your setup. Approval rates range from 85% to 98% depending on the method and provider you use. That gap is not trivial. A 10-point difference in approval rate on high-volume iGaming traffic translates directly to revenue.

Transaction flow time benchmarks by method:

| Payment method | Authorization time | Settlement time | Chargeback risk |

|---|---|---|---|

| Credit/debit card | 2 to 5 seconds | 1 to 3 business days | High |

| Open banking | 3 to 8 seconds | Same day to 24 hours | None |

| Crypto | 10 seconds to 10 minutes | Near-instant to 1 hour | None |

Key functions your payment processing stack must handle include:

- Transaction capture: Collecting and validating payment data at the point of entry

- Intelligent routing: Directing transactions to the acquirer most likely to approve them

- Real-time risk checks: Screening for fraud, velocity abuse, and geo-mismatches before authorization

- Settlement management: Reconciling funds and moving them to your operating accounts

For a deeper look at how these mechanics apply specifically to your sector, the iGaming payments guide covers operator-specific workflows in detail.

Why iGaming and fintech payment processing is considered high-risk

The label "high-risk" is not just a banking formality. It reflects real patterns that make iGaming and fintech genuinely more complex to underwrite and process for.

"iGaming operators face chargeback rates around 0.83% and decline rates above 13%, driven by bonus abuse, friendly fraud, and deposit-withdraw cycling behaviors that standard acquirers are not built to handle."

Chargeback rates average 0.83% in iGaming, which sounds small until you realize that most card networks flag merchants above 0.5% for monitoring programs. Exceeding 1% can get your merchant account terminated entirely.

The specific risk patterns that define this sector include:

- Friendly fraud: Players dispute legitimate charges after losing, claiming unauthorized transactions

- Bonus abuse: Users create multiple accounts to exploit welcome bonuses, then withdraw immediately

- Deposit-withdraw cycling: Rapid fund movement that triggers AML (anti-money laundering) flags

- KYC failures: Incomplete identity verification that exposes operators to regulatory penalties

- Geo-mismatches: Players using VPNs to access platforms from restricted jurisdictions

- Deepfake onboarding: AI-generated identity documents bypassing standard verification tools

These patterns do not just affect fraud losses. They affect your banking relationships, your processing fees, and your ability to maintain merchant accounts at all. Many operators discover this the hard way when their acquirer drops them without warning. The business bank account challenges that iGaming and fintech companies face are directly tied to these risk profiles.

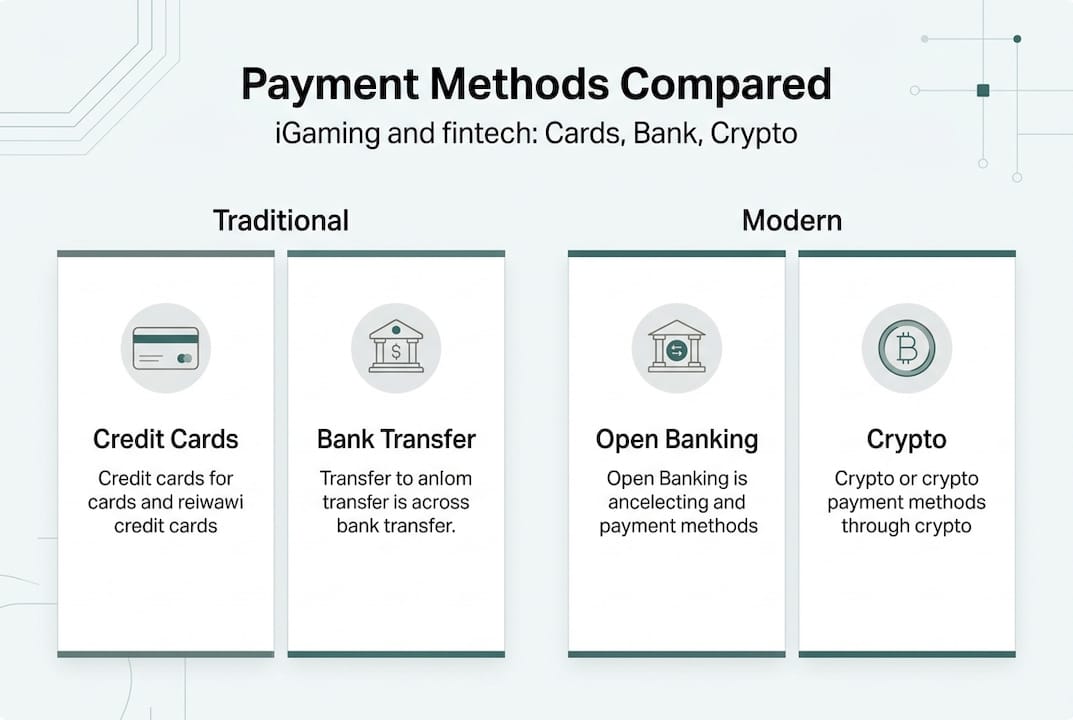

Payment methods compared: Cards, open banking, and crypto

Choosing your payment rails is a strategic decision, not just a technical one. Each method carries different cost structures, risk profiles, and regulatory obligations.

| Method | Processing fees | Approval rate | Chargeback risk | Regulatory complexity |

|---|---|---|---|---|

| Credit/debit card | 1.5% to 3.5% | 85% to 92% | High | Moderate |

| Open banking | 0.1% to 0.5% | 90% to 97% | None | Low to moderate |

| Crypto | 0.1% to 1% | 95% to 99% | None | High (MiCA, VASP) |

Cards remain reliable but carry high-risk profiles, while open banking and crypto offer lower fees and zero chargebacks but introduce their own compliance requirements. Crypto is now mainstream, with 55% of providers supporting it and the sector processing over $81 billion in 2025. Open banking accounts for roughly 20% of deposits on leading platforms.

Pros and cons by method:

Cards:

- Pro: Universal player familiarity, instant authorization

- Con: High chargeback exposure, expensive processing fees, acquirer scrutiny

Open banking:

- Pro: Zero chargebacks, lower fees, faster settlement

- Con: Requires strong bank API coverage in target markets, less familiar to some players

Crypto:

- Pro: Near-zero fees, no chargebacks, global reach without currency conversion

- Con: MiCA compliance in the EU, VASP licensing requirements, price volatility for operators holding crypto

For operators exploring licensing options that align with their payment method mix, the fintech license fee comparison breaks down costs across jurisdictions.

Pro Tip: Do not rely on a single payment method. Payment orchestration, which means routing transactions across multiple PSPs and methods based on real-time performance data, consistently delivers higher approval rates and lower processing costs than any single-rail approach.

Key compliance standards: KYC, AML, and regulatory frameworks

Every payment method you add brings a new layer of regulatory obligation. Compliance is not optional, and it is not a one-time setup. It is an ongoing operational function.

Here are the core compliance processes every iGaming and fintech operator must have in place:

- KYC (Know Your Customer): Verify player identity at onboarding using government-issued ID, proof of address, and increasingly, biometric checks to counter deepfake fraud.

- AML (Anti-Money Laundering): Monitor transaction patterns for structuring, layering, and unusual deposit-withdraw behavior. File Suspicious Activity Reports (SARs) where required.

- Fraud detection: Deploy real-time screening tools that flag velocity abuse, geo-mismatches, and device fingerprint anomalies before transactions complete.

- PEP and sanctions screening: Check customers against politically exposed persons lists and global sanctions databases at onboarding and on an ongoing basis.

- Regulatory reporting: Maintain audit trails and transaction records for the periods required by your licensing jurisdiction, typically five to seven years.

For crypto-specific operations, MiCA and similar regulations are reshaping compliance requirements across the EU and influencing standards globally. MiCA requires crypto asset service providers to register, maintain capital reserves, and implement full AML programs. US operators face FinCEN requirements and state-level money transmission licenses, which vary significantly by state.

The corporate account approval process for iGaming and fintech companies is directly tied to how well your compliance documentation is structured before you approach a bank.

Pro Tip: Investing in compliance infrastructure upfront, before you scale, is dramatically cheaper than retrofitting it after a regulatory action or banking termination. A single AML investigation can cost more than a full year of compliance operations.

Building a resilient payment infrastructure for iGaming and fintech

Knowing the components and risks is one thing. Assembling them into a stack that performs under real operational conditions is another challenge entirely.

Start with your PSP and banking partner selection. Not all PSPs are willing to onboard iGaming or fintech clients, and those that do vary widely in their risk appetite, geographic coverage, and technical capabilities. You need partners who understand your industry, not ones who will terminate your account the moment your chargeback rate ticks up.

Orchestration is the single most impactful architectural decision you can make. By routing transactions dynamically across multiple acquirers and payment methods, you reduce single points of failure and consistently improve approval rates. AI-powered fraud detection now achieves 96.8% accuracy, and fast payouts directly boost player lifetime value, making both capabilities essential components of a modern payment stack.

Your infrastructure must include:

- Multi-acquirer routing: Automatic failover when one acquirer declines or goes offline

- Real-time fraud scoring: Transaction-level risk assessment before authorization, not after

- Rapid payout capability: Sub-24-hour withdrawals, which are now a baseline player expectation

- Robust KYC tooling: Automated document verification with liveness detection to counter deepfake fraud

- Real-time analytics dashboard: Visibility into approval rates, decline reasons, and chargeback trends by method and geography

- Compliance audit trails: Automated record-keeping that satisfies regulatory reporting requirements

Finally, treat your payment stack as a living system. Regulations change, new payment methods emerge, and acquirer risk appetites shift. Schedule quarterly audits of your processing performance and compliance posture. For operators considering their banking setup, opening accounts for iGaming in jurisdictions like Hong Kong offers specific structural advantages worth understanding.

Partnering for success: How Deincepstart can help

Building compliant payment infrastructure for iGaming or fintech is not something you want to figure out through trial and error. The cost of getting it wrong, whether through a terminated merchant account, a regulatory action, or a banking relationship that collapses at the worst moment, is simply too high.

At Deincepstart, we work directly with iGaming operators, fintech founders, and crypto businesses to build the financial infrastructure that supports real growth. That means helping you open corporate bank accounts in the right jurisdictions, structure your entity for payment processing approval, obtain EMI and VASP licenses, and design a payment stack that meets compliance requirements without sacrificing performance. If you are ready to stop guessing and start building with a team that understands your industry, reach out for a personalized consultation. We have helped operators across BVI, Cayman, Seychelles, Mauritius, and Hong Kong get their infrastructure right from the start.

Frequently asked questions

What does a payment processor do in the context of iGaming?

A payment processor routes, verifies, and settles transactions between players, operators, and banks, managing risk and regulatory checks at every step. In iGaming, this also includes real-time fraud screening and chargeback management that standard processors are not equipped to handle. Payment processing workflows in iGaming are significantly more complex than in standard e-commerce.

Which payment methods have the lowest decline and chargeback rates?

Open banking and crypto consistently deliver lower fees and zero chargeback exposure, while card methods see decline rates above 13% and meaningful chargeback risk. The right mix depends on your player base and target markets.

What are the main compliance risks when processing for iGaming or fintech?

Operators must maintain KYC, AML, and fraud detection programs, and MiCA and related standards are adding new layers of complexity for crypto and open banking operations. Failing to meet these requirements can result in banking termination or regulatory penalties.

How fast can iGaming payment processing work for payouts?

With the right infrastructure and payment partners, payouts under 24 hours are achievable and have been shown to boost player lifetime value by 1.5 to 2 times compared to slower payout operators.