Banks turn away fintech and iGaming companies at staggering rates. 50-85% rejection rates mean most operators hit a wall before they ever process a single transaction. The reasons range from chargeback exposure to murky ownership structures, and most founders walk into the process completely unprepared. This guide walks you through every stage of opening a corporate bank account for a high-risk business, from understanding why banks say no to building the compliance narrative that gets you to yes. If you run a fintech startup, iGaming platform, or crypto-adjacent operation, this is the roadmap you need.

Table of Contents

- Understand high-risk banking challenges

- Prepare your documentation and compliance framework

- Step-by-step process for account application

- Troubleshooting and boosting approval odds

- Our perspective: What most guides miss about high-risk banking success

- Get expert help for your fintech or iGaming bank account setup

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Preparation is key | Having the right documents and compliance framework greatly increases your chances of approval. |

| EMIs increase approval odds | Electronic Money Institutions approve 65-80% of high-risk fintech and iGaming applications. |

| Prioritize compliance | Poor compliance leads to de-banking, so robust AML and KYC are essential from the start. |

| Learn from each attempt | Bank rejections are common; adapt and improve your application using feedback for better success moving forward. |

Understand high-risk banking challenges

Not all businesses are treated equally by banks. Fintech companies, iGaming operators, online gambling platforms, and crypto-adjacent businesses fall into a category that compliance teams flag automatically. Banks see these sectors as carrying elevated exposure across multiple risk dimensions, and that shapes every interaction you will have with a financial institution.

The core problem is chargeback rates. High-risk industries typically generate chargeback rates of 5-12%, compared to under 1% for standard retail businesses. Add in anti-money laundering (AML) scrutiny, cross-border transaction complexity, and the involvement of multiple payment processors, and you have a profile that most bank compliance officers would rather decline than approve.

Here is what that looks like in practice:

| Factor | Standard Business | High-Risk Business |

|---|---|---|

| Chargeback rate | Under 1% | 5-12% |

| AML scrutiny level | Standard | Enhanced |

| Approval rate (traditional bank) | 70-90% | 15-50% |

| Approval rate (EMI) | 80-95% | 65-80% |

| Typical onboarding time | 1-2 weeks | 4-16 weeks |

Banks also worry about regulatory exposure. If your business operates under a license from a jurisdiction the bank does not recognize, or if your ultimate beneficial owners (UBOs) are difficult to verify, the application stalls immediately. The iGaming banking landscape is particularly unforgiving because regulators in multiple countries scrutinize these operators simultaneously.

What banks actually want to see before approving a high-risk account:

- Clear UBO structure with verified identities and source of funds

- Active AML and KYC policies with a named compliance officer

- Valid gaming or financial services license from a recognized authority

- Detailed breakdown of the business model, revenue streams, and transaction flows

- Evidence of ongoing compliance training and internal audit procedures

"Banks reject 50-85% of high-risk iGaming and fintech applications due to chargebacks, AML risks, and lack of clear compliance documentation."

Understanding this upfront changes how you approach the process. You are not just filling out a form. You are making a case that your business is manageable risk. Our fintech compliance guide covers the regulatory layer in more detail if you want to go deeper before moving forward.

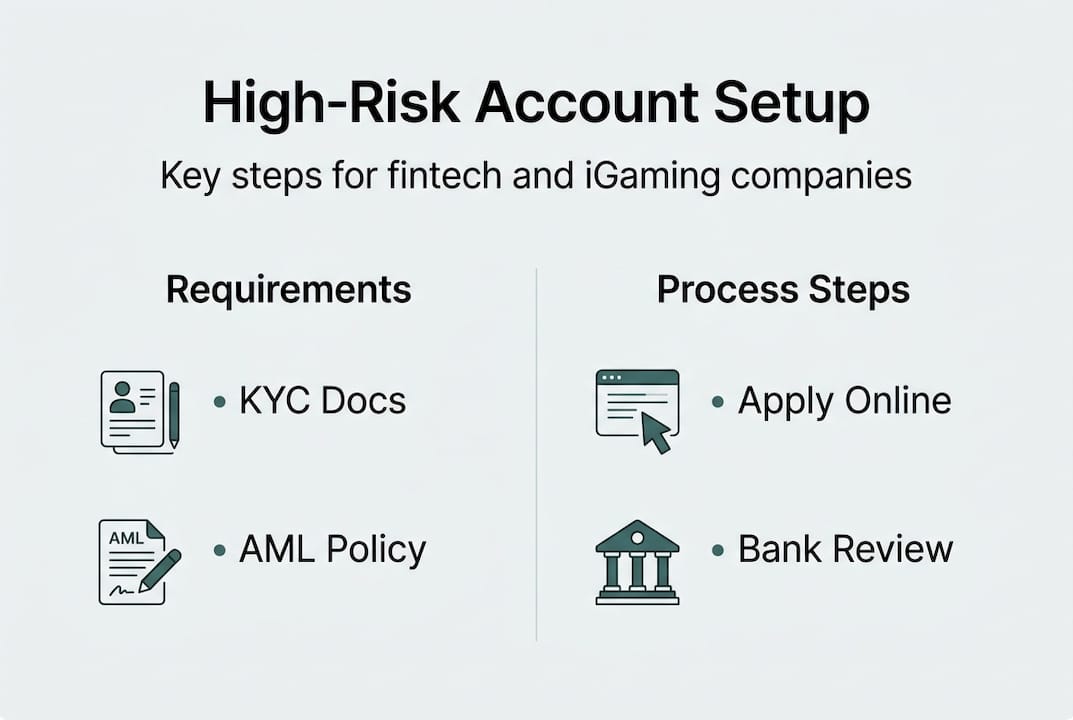

Prepare your documentation and compliance framework

Most applications fail not because the business is illegitimate, but because the documentation is incomplete or inconsistent. Banks conducting enhanced due diligence (EDD) on high-risk applicants need a specific set of materials, and gaps in any area trigger delays or outright rejections.

Here is the complete list of what you need to prepare:

- Certificate of incorporation and corporate registry documents

- UBO register with certified identification and source of wealth declarations

- Valid operating license (gaming authority, financial services regulator, or equivalent)

- AML policy document, including transaction monitoring procedures

- KYC procedures manual with customer onboarding and verification steps

- Business plan with revenue model, target markets, and projected transaction volumes

- Transaction flow diagrams showing how funds move through your platform

- Risk assessment report covering your customer base and geographic exposure

- Bank reference letters or financial statements from prior accounts

- Compliance officer appointment letter and credentials

Pro Tip: Create a visual flowchart of your transaction lifecycle. Show exactly how a customer deposit enters your system, how it is held, and how withdrawals are processed. Banks respond well to clarity, and a one-page diagram often communicates more than ten pages of text.

The banking and compliance guide we put together goes into the specific formatting banks prefer for AML documentation. Getting the structure right matters as much as having the policies in place.

Here is a comparison of what standard vs. enhanced due diligence requires:

| Document | Standard KYC | Enhanced Due Diligence (High-Risk) |

|---|---|---|

| ID verification | Yes | Yes, plus source of funds |

| Business license | Optional | Mandatory |

| AML policy | Not required | Required, detailed |

| Transaction flow diagram | Not required | Strongly recommended |

| Compliance officer details | Not required | Required |

Enhanced due diligence requires AML policy, KYC procedures, transaction monitoring evidence, licensing proof, UBO transparency, and a detailed business model. Treat this as a minimum, not a ceiling. The more clearly you can demonstrate that your compliance framework is operational (not just on paper), the stronger your application becomes. Our corporate banking solutions page outlines how we help structure these packages for different jurisdictions.

Step-by-step process for account application

With your documentation ready, the application process becomes a structured sequence rather than a guessing game. Here is how to move through it efficiently:

- Choose your provider type. Decide between a traditional bank and an Electronic Money Institution (EMI). EMIs offer approval rates of 65-80% compared to 15-50% at traditional banks. For most new high-risk operators, starting with an EMI is the smarter path.

- Select jurisdiction and provider. Match your business structure to the banking jurisdiction. A BVI holding company may work well with a European EMI, but a Malta-licensed iGaming operator needs a bank familiar with MGA-regulated businesses.

- Complete the onboarding forms. Fill out all KYC forms accurately. Inconsistencies between your application and your corporate documents are one of the most common triggers for rejection.

- Submit your full due diligence pack. Include every document from the checklist above. Submit as a single organized package, not in pieces.

- Prepare for the compliance interview. Most banks and EMIs conduct a video or written Q&A. Expect questions about your customer base, transaction volumes, chargeback management, and AML controls.

- Respond to follow-up requests promptly. Delays in responding signal disorganization. Aim to reply within 24-48 hours.

- Account setup and testing. Once approved, complete any remaining verification steps and run a small test transaction before going live.

Pro Tip: Tailor your business narrative to the specific institution's risk appetite. A bank that serves other gaming companies will respond differently to your application than a generalist bank seeing iGaming for the first time. Research your target institution before applying.

Applications get flagged most often for three reasons: an incomplete business case, a mismatch between your offshore structure and the bank's accepted jurisdictions, or missing compliance policies. Our account approval strategies guide covers how to address each of these before they become problems. If you are building out payment infrastructure alongside the account, the payment processing guide is worth reading in parallel.

Troubleshooting and boosting approval odds

Rejection is common. It is not the end of the road. What separates operators who eventually get approved from those who keep hitting walls is how they respond to setbacks.

The most frequent reasons applications fail:

- Missing or outdated AML and KYC documentation

- UBO structure that is unclear or involves jurisdictions the bank avoids

- No named compliance officer or evidence of internal controls

- Business model that the bank does not understand or cannot categorize

- Prior banking relationships that ended badly or accounts that were closed

- Operating in a geography flagged as high-risk by the bank's own policies

If you receive a rejection, request specific feedback whenever possible. Some institutions will not provide detailed reasons, but many will. Use that feedback to identify the exact gap and address it before resubmitting.

"Fintech and iGaming entrepreneurs should prioritize compliance. Poor AML controls can lead to de-banking with as little as 30-90 days notice."

This is not a theoretical risk. De-banking mid-operation is catastrophic for an iGaming or fintech business. It freezes player funds, disrupts payment flows, and can trigger regulatory scrutiny. The best protection is building compliance that is genuinely operational, not just documented.

For multi-account structures, separate your operating account from your players' funds account. This is both a best practice and a requirement in many regulated jurisdictions. It also makes your banking relationships easier to manage because each account has a clear, single purpose.

When a traditional bank is not the right fit, consider:

- European or Asian EMIs with explicit high-risk programs

- Jurisdictions with more accommodating banking frameworks (Lithuania, Georgia, Hong Kong)

- Compliance consultancies with existing bank relationships

Our account verification best practices resource covers the operational side of keeping accounts in good standing once you are approved.

Our perspective: What most guides miss about high-risk banking success

After working through dozens of high-risk banking applications across iGaming, fintech, and crypto sectors, we have noticed a consistent pattern. Founders who fail usually have the documents. What they lack is a coherent narrative.

Banks do not just read your AML policy. They read your business. They look at whether the story you are telling is internally consistent, whether your transaction volumes match your stated customer base, and whether your compliance setup reflects a business that actually operates the way you claim. A polished document package with a weak or contradictory business case will still get rejected.

The uncomfortable truth is that banks are looking for red flags in substance, not just in paperwork. A founder who can explain their chargeback management process in a five-minute call will outperform one who submits a 40-page compliance manual but cannot answer basic questions about their operations.

Transparency and relationship-building matter more than most guides acknowledge. The importance of ongoing compliance is not just about avoiding de-banking. It is about building the kind of track record that makes future applications faster and easier. Treat your banking relationship as a long-term asset, not a one-time transaction.

Get expert help for your fintech or iGaming bank account setup

Navigating high-risk banking without the right support costs time, money, and momentum. Most operators who come to us have already faced at least one rejection and are looking for a more structured approach.

At Deincepstart, we support fintech companies and iGaming operators through every stage of the banking process: structuring your compliance documentation, identifying the right banking partners for your jurisdiction and business model, and managing the application from submission to approval. We also help with offshore structuring, EMI licensing, and ongoing compliance maintenance. If you are ready to move forward with a bank account setup that is built to succeed, reach out to our team for a consultation.

Frequently asked questions

Why do banks reject so many fintech or iGaming account applications?

Banks classify fintech and iGaming as high-risk due to elevated chargebacks, complex AML exposure, and regulatory scrutiny, resulting in 50-85% rejection rates across standard application processes.

What documents and policies do I need for a high-risk bank account setup?

You need a complete enhanced due diligence package including AML policy, KYC procedures, transaction monitoring evidence, licensing proof, UBO register, and a detailed business model with transaction flow diagrams.

Is it better to use a traditional bank or an EMI for high-risk accounts?

EMIs approve 65-80% of applications while traditional banks approve only 15-50%, making EMIs a significantly more reliable starting point for high-risk fintech and iGaming operators.

What can I do if my application is rejected?

Request feedback from the institution, identify the specific compliance gap, strengthen your documentation or business narrative, and consider resubmitting or approaching an EMI with a specialized high-risk program.