Compliance costs the global financial industry over $200 billion annually, and 93% of fintechs report serious regulatory struggles. Yet most founders still treat compliance as a legal checkbox rather than a core operational function. That mindset is expensive. False positives in AML screening run between 85% and 95%, KYC failures plague 70% of fintechs, and compliance can consume 5 to 15% of total revenue. This guide cuts through the noise and gives you a practical, structured approach to fintech compliance, covering frameworks, regulatory requirements, high-risk industry nuances, and the mistakes that sink otherwise solid businesses.

Table of Contents

- Why fintech compliance matters: Risks, regulations, and reality

- Core compliance frameworks for fintech: Methodologies and pillars

- Regulatory landscape: US and global requirements

- High-risk industry nuances: Adult, borders, vIBANs, and gaming

- Common mistakes and practical solutions: Applying compliance best practices

- How Deincepstart supports fintech compliance

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Frameworks matter most | Fintech compliance rests on structured risk assessment, AML programs, and compliance-by-design. |

| Know regulators and rules | Understanding federal, state, and global requirements is essential for banking and payments compliance. |

| High-risk protocols are critical | Enhanced due diligence and multi-party accountability are required for adult, border, gaming, and vIBAN operations. |

| Avoid classic mistakes | Over-compliance can be as damaging as under-compliance; build controls that balance innovation and risk. |

| Expert help accelerates success | Operationalizing compliance frameworks with expert partners can reduce cost, risk, and product friction. |

Why fintech compliance matters: Risks, regulations, and reality

Compliance is not just about avoiding fines. It is about staying in business. Banks de-risk clients who cannot demonstrate clean AML and KYC programs. Payment processors drop merchants who fail audits. Regulators revoke licenses. The consequences are operational, not just legal.

The EU EBA reports that 70% of supervisory authorities identify high money laundering and terrorist financing risks in fintech, largely because growth has outpaced compliance infrastructure. But the EBA also flags the opposite problem: over-compliance leads to de-risking innocent customers, cutting off legitimate businesses from banking access.

"The challenge is not just doing more compliance. It is doing the right compliance, calibrated to actual risk, not perceived risk."

For founders building in high-risk sectors, this balance is critical. You need enough controls to satisfy regulators and banking partners, but not so many that you create friction that kills your product. Understanding the compliance startup guide basics is the first step toward that balance.

Here are the most common compliance pitfalls for fintechs:

- Treating KYC as a one-time onboarding step rather than an ongoing process

- Failing to document AML policies in a format regulators can audit

- Ignoring transaction monitoring until a suspicious activity report is triggered

- Underestimating the compliance requirements tied to corporate banking for fintechs

- Assuming offshore structures eliminate compliance obligations

- Not assigning a dedicated compliance officer until after a regulatory inquiry

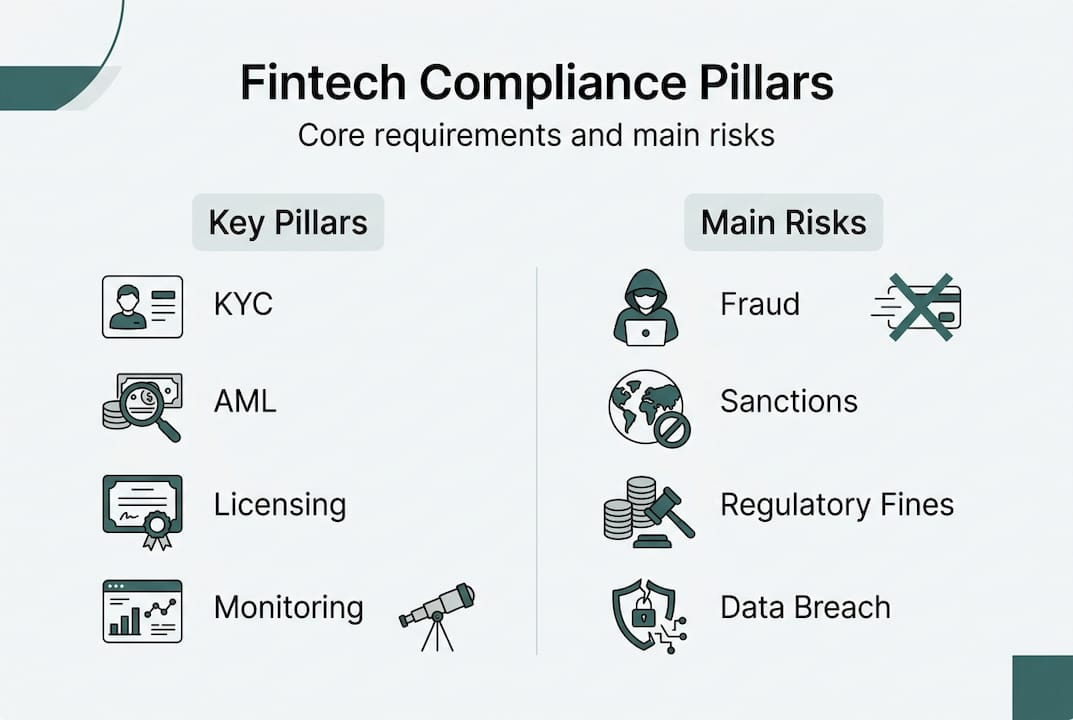

Core compliance frameworks for fintech: Methodologies and pillars

A solid compliance program is not a single policy document. It is an architecture. The core methodologies include risk assessments, robust AML programs built on five pillars, transaction monitoring, and compliance-by-design architecture embedded into your product from day one.

The five AML pillars are:

- Written policies and procedures that reflect your actual business model

- Ongoing employee training tied to real scenarios, not generic modules

- Independent testing and auditing of your controls at regular intervals

- A designated compliance officer with real authority and accountability

- Customer due diligence (CDD) and enhanced due diligence (EDD) protocols

Modern fintechs are moving beyond static rule-based systems. Event-driven architecture and RegTech AI reduce false positives and allow compliance to scale with transaction volume without proportionally scaling headcount. This is the difference between a compliance program that grows with your business and one that becomes a bottleneck.

| Feature | Traditional compliance | Modern AI-enabled compliance |

|---|---|---|

| Monitoring approach | Rule-based, static thresholds | Event-driven, adaptive models |

| False positive rate | 85 to 95% | Significantly reduced |

| Scalability | Manual, headcount-dependent | Automated, scales with volume |

| Audit readiness | Periodic, document-heavy | Continuous, real-time logs |

| Cost profile | High fixed costs | Lower marginal cost at scale |

Pro Tip: Do not wait until your product is live to build compliance controls. Integrate KYC flows, transaction monitoring hooks, and audit logging into your first working prototype. Retrofitting compliance into a live product costs three to five times more than building it in from the start.

For a deeper look at how this applies to payments specifically, the payment processing compliance guide covers the operational layer in detail.

Regulatory landscape: US and global requirements

The US regulatory environment for fintech is fragmented by design. Federal oversight comes from FinCEN (anti-money laundering), the CFPB (consumer protection), and the OCC (national bank charters). But payments also require state-level licensing.

Money Transmitter Licenses are required state-by-state for any business moving money, and the process takes 12 to 24 months per state. If you plan to operate nationally, you are looking at a multi-year licensing campaign with significant legal and filing costs.

| Requirement | Jurisdiction | Timeline | Key regulator |

|---|---|---|---|

| Money Transmitter License | US (state-by-state) | 12 to 24 months per state | State regulators |

| Bank Secrecy Act / AML program | US federal | Ongoing | FinCEN |

| EMI license | EU / UK | 6 to 18 months | National regulators |

| VASP registration | EU (MiCA) | 3 to 12 months | National regulators |

| GDPR compliance | EU | Ongoing | Data protection authorities |

Compliance costs as a share of revenue are not trivial. For early-stage fintechs, compliance can represent 10 to 15% of operating expenses before the business reaches scale. That number drops as revenue grows, but it never disappears.

For founders exploring licensing options beyond the US, fintech license examples for high-risk startups covers jurisdictions like Seychelles, Mauritius, and BVI. And if your model involves moving money across borders, cross-border payment solutions for iGaming and fintech is worth reviewing before you structure your entity.

High-risk industry nuances: Adult, borders, vIBANs, and gaming

High-risk industries do not just face more compliance scrutiny. They face different compliance requirements entirely. The controls that work for a B2B SaaS payments company will not satisfy regulators reviewing an adult content platform or an iGaming operator.

Adult payment processing requires enhanced KYC and AML, plus content verification obligations under 18 U.S.C. §2257. Border logistics companies face cartel exposure risk, which demands EDD on counterparties and transaction routes. Virtual IBANs (vIBANs) carry elevated ML/TF risk because they can obscure the true originator of funds.

Here are the key compliance scenarios and controls for high-risk sectors:

- iGaming operators: Geolocation verification, player source-of-funds checks, responsible gambling controls, and licensing in each target jurisdiction

- Adult platforms: Age verification, content compliance documentation, enhanced AML screening for high-volume micropayments

- Border logistics: EDD on all counterparties, sanctions screening, and transaction route documentation

- vIBAN providers: Originator transparency requirements, nested account monitoring, and clear liability assignment

- Crypto businesses: VASP registration, travel rule compliance, and wallet screening

Multi-party risk in bank-fintech partnerships is one of the most overlooked compliance gaps. When a bank, a fintech, and a payment processor are all involved in a transaction, Regulation E errors and AML failures can fall through the cracks between parties. Assign accountability in writing before you go live.

Pro Tip: In any multi-party payment arrangement, document exactly which entity owns each compliance obligation. Verbal agreements do not hold up in regulatory inquiries. A one-page responsibility matrix signed by all parties is worth more than a 50-page contract with vague language.

For operators specifically, the iGaming payment compliance guide and the Hong Kong banking for gaming overview are practical starting points.

Common mistakes and practical solutions: Applying compliance best practices

Most compliance failures are not caused by bad intentions. They are caused by bad sequencing. Founders build the product, then try to bolt compliance on afterward. By that point, the architecture does not support it, the team is not trained for it, and the cost is punishing.

Over-compliance is also a real risk. Applying maximum scrutiny to every customer regardless of actual risk profile creates friction, drives away legitimate users, and wastes resources that should be focused on genuine threats. The goal is calibrated compliance, not maximum compliance.

"Compliance-by-design is not about adding more gates. It is about building the right gates in the right places, so the product works smoothly for legitimate users and flags the right risks automatically."

Here is a practical action list for fintech founders:

- Conduct a formal risk assessment before you write a single line of compliance policy

- Hire or appoint a compliance officer before your first external funding round

- Build KYC and transaction monitoring into your product architecture from the first sprint

- Document every compliance decision with a rationale that survives regulatory review

- Test your AML controls with independent auditors at least annually

- Review your compliance program every time you enter a new market or add a new product line

For founders still working through fintech business bank accounts and banking relationships, the corporate account approval guide walks through exactly what banks look for before approving high-risk fintech accounts.

How Deincepstart supports fintech compliance

Building a compliant fintech operation in a high-risk sector is not something most founders should navigate alone. The regulatory landscape is fragmented, the stakes are high, and the cost of getting it wrong compounds quickly.

Deincepstart works directly with iGaming operators, crypto businesses, and fintech founders to operationalize compliance from the ground up. We help you open corporate bank accounts with institutions that understand your industry, structure offshore entities in BVI, Cayman, Seychelles, and Mauritius, obtain EMI and VASP licenses, and build payment infrastructure that satisfies regulators without killing your product. If you are ready to stop guessing and start building with a clear compliance roadmap, reach out to our team for a direct consultation.

Frequently asked questions

What are the core elements of fintech compliance?

Risk assessments, AML controls, transaction monitoring, and compliance-by-design architecture are the foundational pillars. A designated compliance officer and documented CDD/EDD protocols complete the program.

How long does it take to obtain a Money Transmitter License (MTL) in the United States?

MTL processing takes 12 to 24 months per state, depending on your business model and the specific state's requirements. National coverage requires a multi-year licensing strategy.

What are enhanced due diligence (EDD) requirements for high-risk industries?

High-risk sectors require rigorous KYC and AML, content verification for adult platforms, and clearly documented multi-party accountability across all payment relationships.

Why do fintechs struggle with compliance and KYC?

Most fintechs lack the frameworks and infrastructure to handle high false positive rates and evolving regulatory requirements, which drives up costs and creates operational bottlenecks.

Is over-compliance a risk for fintechs?

Yes. The EBA has flagged that over-compliance leads to de-risking legitimate customers, creating access barriers and operational inefficiencies that harm both businesses and their users.