Corporate account verification is not a formality. For iGaming operators, fintech companies, and crypto businesses, it is the single most consequential step between your company and a functioning bank account or payment processing relationship. Most rejections and delays we see at Deincepstart trace back to the same root cause: teams treating verification as a checklist rather than a risk management process. Regulatory harmonization demands more rigorous KYB processes with severe penalties for non-compliance, and the stakes have never been higher. This article breaks down what corporate account verification actually involves, how the process works end to end, and what separates companies that sail through from those that stall.

Table of Contents

- What is corporate account verification?

- Why is corporate account verification required?

- How the corporate account verification process works

- Common challenges and pitfalls in account verification

- Best practices for successful verification in regulated industries

- Deincepstart: Simplifying corporate account verification

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| KYB is critical | Corporate account verification is a regulatory necessity to prevent fraud and money laundering. |

| Primary sources matter | Relying on original documents and strong audit trails safeguards against regulatory penalties. |

| Automate for efficiency | Leveraging automation and clear policies reduces errors and approval times. |

| Avoid common pitfalls | Incomplete records or non-uniform processes often result in costly verification failures. |

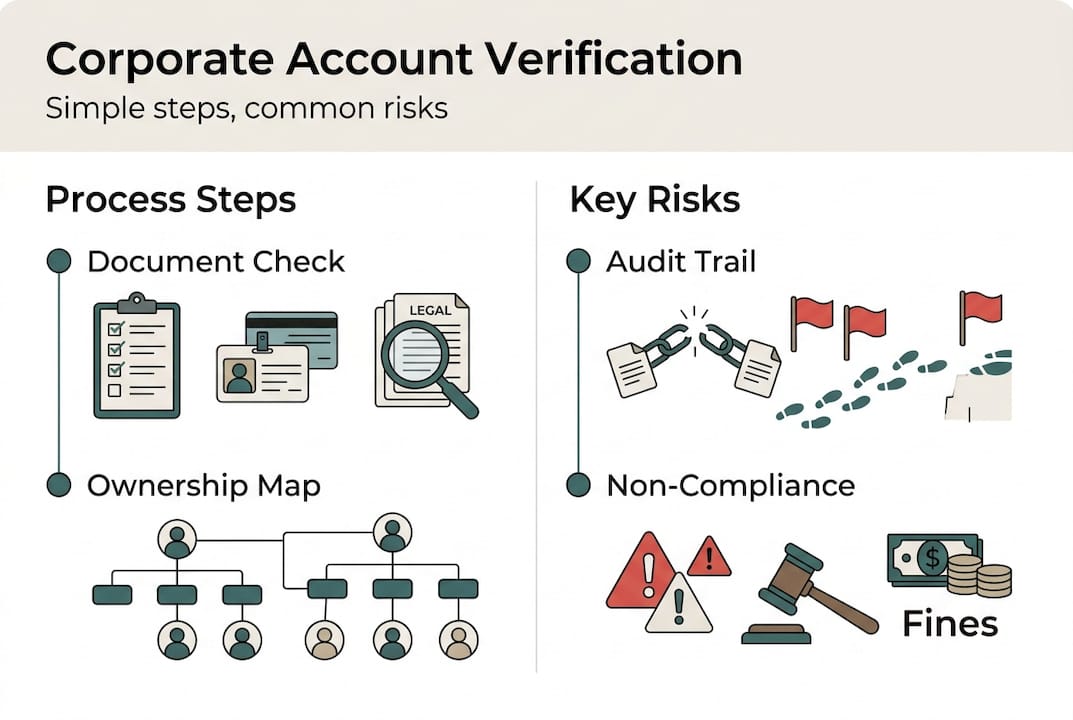

What is corporate account verification?

Corporate account verification is the process financial institutions use to confirm that a business is legally registered, operationally legitimate, and not a vehicle for financial crime. It goes well beyond checking a company name. Banks and payment processors need to understand who owns the business, who controls it, and what risk profile it carries before they extend any financial services.

This process sits at the core of Know Your Business (KYB) frameworks, which are the corporate equivalent of Know Your Customer (KYC). KYB is mandated under anti-money laundering (AML) regulations across virtually every major financial jurisdiction. Uniform KYB standards are increasingly mandated for regulated entities, meaning there is less room than ever to cut corners or rely on informal arrangements.

For iGaming operators, fintech startups, and cryptocurrency businesses, the stakes are compounded. These industries carry elevated risk classifications by default. That means verification requirements are stricter, documentation thresholds are higher, and the margin for error is essentially zero. A well-prepared application reviewed in our corporate account approval guide can make the difference between a 30-day approval and a 6-month rejection cycle.

Here is what corporate account verification typically covers:

- Legal status confirmation: Is the company validly incorporated and in good standing?

- Ownership mapping: Who are the ultimate beneficial owners (UBOs) holding 10% or more?

- Director identification: Are all directors verified individuals with clean compliance records?

- Business activity review: Does the declared business model match actual operations?

- Risk classification: Does the company operate in a high-risk sector, jurisdiction, or both?

Pro Tip: If your company has a complex ownership structure with holding companies or nominee arrangements, map the full UBO chain before you approach any bank. Institutions will ask for it, and an incomplete answer triggers enhanced due diligence automatically.

Why is corporate account verification required?

The short answer is that banks and payment processors are legally obligated to conduct it. The longer answer is that the consequences of skipping it are severe enough that no regulated institution will take the risk.

KYB and AML regulations require financial institutions to verify every corporate client before onboarding and to monitor them on an ongoing basis. Failure to do so exposes the institution to regulatory action. But here is what many business owners miss: the obligation flows downstream. If your company cannot provide adequate documentation, the bank cannot onboard you without violating its own compliance obligations. The rejection is not personal. It is structural.

"Audit trails and primary sources are essential to meet modern compliance standards and avoid penalties." Institutions that rely on secondary or unverifiable sources face the same regulatory exposure as those that skip verification entirely.

The financial penalties for non-compliance are not abstract. Fines can reach up to 10% of annual turnover for serious breaches, and enforcement actions have increased sharply across the EU, UK, and Asia-Pacific regions. Beyond fines, there is the operational risk: accounts frozen, payment rails suspended, and business continuity threatened.

For companies in regulated industries, the risks multiply. Understanding fintech compliance essentials is not optional reading. Neither is staying current on payment processing compliance requirements, which evolve faster than most internal legal teams can track.

Key reasons verification is non-negotiable:

- Regulatory obligation: Banks face direct liability for inadequate KYB.

- Fraud prevention: Verification catches shell companies and fraudulent actors before they access financial infrastructure.

- Reputational protection: A single high-profile compliance failure can cost an institution its operating license.

- Business continuity: For your company, passing verification is the prerequisite for everything else.

How the corporate account verification process works

The process is more structured than most applicants expect. Understanding each stage helps you prepare the right materials and avoid the delays that come from submitting incomplete packages.

Here is the typical end-to-end flow:

- Data collection: The institution collects basic company information, including registered name, jurisdiction, business activity, and ownership structure.

- Document submission: You provide primary source documents to support the data collected.

- Risk assessment: The compliance team classifies your company by risk level based on industry, jurisdiction, and ownership complexity.

- Documentation validation: Each document is verified against primary sources, including government registries and official databases.

- Source of funds review: For higher-risk entities, the institution will request evidence of how the business generates revenue.

- Approval or escalation: Standard-risk companies proceed to approval. Higher-risk companies enter enhanced due diligence (EDD), which involves additional documentation and sometimes a compliance interview.

- Periodic review: Approved accounts are re-verified on a scheduled cycle, typically every 12 to 24 months.

Primary source documentation is central for effective KYB and streamlined approvals. Secondary sources, such as third-party summaries or unverified copies, are increasingly rejected by compliance teams operating under tighter standards.

The table below shows the most commonly required documents by document type and purpose:

| Document | Purpose | Notes |

|---|---|---|

| Certificate of incorporation | Confirms legal existence | Must be current and apostilled if cross-border |

| Shareholder register | Maps ownership structure | Must show all UBOs above threshold |

| Proof of registered address | Confirms operational presence | Utility bill or official registry extract |

| Director identification | Verifies individual identities | Passport plus proof of address |

| AML/KYC policy | Demonstrates internal controls | Required for fintech and crypto applicants |

| Source of funds declaration | Explains revenue origin | Supported by bank statements or audited accounts |

For companies operating across multiple jurisdictions, understanding the specific requirements for each market is critical. Our resources on bank account checks and corporate banking solutions cover jurisdiction-specific nuances in detail.

Pro Tip: Request a pre-submission checklist from the institution before you compile your documents. Many banks publish their KYB requirements internally but do not share them proactively. Asking directly saves weeks of back-and-forth.

Common challenges and pitfalls in account verification

Even well-prepared companies run into problems. The most common issues are predictable, which means they are also preventable.

Relying on non-primary sources and incomplete audit trails can put firms at serious regulatory risk. This is the single most frequent cause of delays we see. A company submits a shareholder register that does not match the incorporation documents, or provides a director ID that has expired, and the entire application stalls while corrections are requested.

Here is a comparison of common pitfalls versus the correct approach:

| Common mistake | Correct approach |

|---|---|

| Submitting photocopies without certification | Provide certified true copies or notarized originals |

| Incomplete UBO disclosure | Map every ownership layer above the threshold |

| Outdated company structure documents | Update registry filings before applying |

| Mismatched addresses across documents | Ensure all documents reflect the same registered address |

| Missing AML policy for regulated entities | Prepare a compliant internal AML framework in advance |

Beyond documentation errors, structural issues create the most serious delays. Companies with nominee directors, complex holding structures, or recent ownership changes face heightened scrutiny. This is especially true for businesses seeking high-risk startup licensing or those exploring banking in Hong Kong, where compliance standards are rigorous.

Best practices to avoid common pitfalls:

- Centralize your compliance data: Keep a single, updated repository of all corporate documents with version control.

- Train your team: Compliance staff should understand what constitutes a primary source and why it matters.

- Audit your own application: Before submission, run an internal review against the institution's stated requirements.

- Document your processes: Regulators and banks want to see that your compliance function is systematic, not reactive.

Best practices for successful verification in regulated industries

High-performing compliance teams in iGaming, fintech, and crypto share a few consistent habits. They do not treat verification as a one-time event. They build it into their operational rhythm.

Here is a practical framework for scalable, compliant verification:

- Establish a unified KYB policy: Document your internal standards for corporate verification, including document requirements, review timelines, and escalation procedures. This policy should align with the jurisdictions where you operate.

- Implement automated document validation: Manual document checks are slow and error-prone. Automated tools can verify document authenticity, cross-reference registry data, and flag inconsistencies in real time.

- Schedule regular framework audits: Your KYB framework should be reviewed at least annually. Regulatory standards shift, and a framework that was compliant in 2024 may have gaps by 2026.

- Train compliance teams annually: Regulations evolve. Staff who were trained two years ago may be operating on outdated assumptions. Annual training is not optional in high-risk industries.

Harmonizing KYB procedures and prioritizing auditable primary sources reduces failure rates and fines. Companies that build this discipline into their operations consistently outperform those that treat compliance as a reactive function.

For companies managing cross-border payments or navigating iGaming payments compliance, the verification framework must account for multiple regulatory environments simultaneously. That requires both a strong internal policy and access to jurisdiction-specific expertise.

Additional best practices worth embedding:

- Assign clear ownership: One person or team should own the KYB process end to end. Shared responsibility creates gaps.

- Build in re-verification triggers: Do not wait for the scheduled review cycle. Any significant company change, such as a new director, ownership transfer, or new business line, should trigger an immediate review.

- Maintain an audit trail for every decision: Document why each verification decision was made, not just what was decided.

Pro Tip: If you operate in multiple jurisdictions, map your KYB requirements by market and identify the highest common denominator. Building your compliance framework to the strictest standard means you are automatically compliant in less demanding markets.

Deincepstart: Simplifying corporate account verification

For companies seeking to future-proof their compliance and verification processes, specialized help is available. At Deincepstart, we work directly with iGaming operators, fintech companies, and crypto businesses to prepare and execute corporate account verification that meets the standards of banks and payment processors across multiple jurisdictions.

Our team has guided clients through verification processes in Hong Kong, the EU, and offshore jurisdictions including BVI, Cayman, and Mauritius. We know what compliance teams look for, what triggers enhanced due diligence, and how to structure your documentation to minimize delays. Whether you are opening your first corporate account or rebuilding a compliance framework that has failed inspection, our corporate verification solutions are built around your specific industry and risk profile. Reach out to discuss your situation and get a clear picture of what your verification process should look like.

Frequently asked questions

What are the key documents required for corporate account verification?

Most banks require a certificate of incorporation, proof of address, shareholder registry, and identification for all directors and beneficial owners. Primary source documentation is essential, meaning certified originals or notarized copies rather than unverified scans.

How often do companies need to re-verify their corporate accounts?

Periodic review is required typically every 12 to 24 months, though significant company changes such as new ownership or a new business line should trigger an immediate re-verification regardless of the scheduled cycle.

What happens if KYB requirements aren't met during verification?

Failure can result in application rejection, account suspension, or regulatory fines for the institution. For your business, penalties up to 10% of turnover are possible if your own compliance obligations are found to be inadequate.

Can automated tools reduce errors in corporate account verification?

Yes. Automated document validation tools minimize manual errors, accelerate cross-referencing against official registries, and create the audit trails that regulators and banks require for compliant onboarding.